Econometrics Toolbox

Modéliser et analyser des systèmes économiques et financiers avec des méthodes statistiques d’analyse de séries temporelles

Vous avez des questions ? Contacter un commercial.

Vous avez des questions ? Contacter un commercial.

Econometrics Toolbox propose des fonctions et des workflows interactifs pour analyser et modéliser des séries temporelles. La toolbox offre un large éventail de visualisations et de diagnostics pour la sélection de modèles, notamment des tests d'autocorrélation et d'hétéroscédasticité, de racine unitaire et de stationnarité, de cointégration, de causalité et de changement structurel. Vous pouvez estimer, simuler et prévoir des systèmes économiques avec une variété de frameworks de modélisation, utilisables soit de manière interactive avec l'application Econometric Modeler, soit de manière programmatique avec des fonctions offertes par la toolbox. Ces multiples frameworks incluent des modèles de régression, ARIMA, de représentation d'état, GARCH, VAR et VEC multivariés et à commutation. La toolbox offre également des outils bayésiens pour développer des modèles variables dans le temps qui exploitent de nouvelles données.

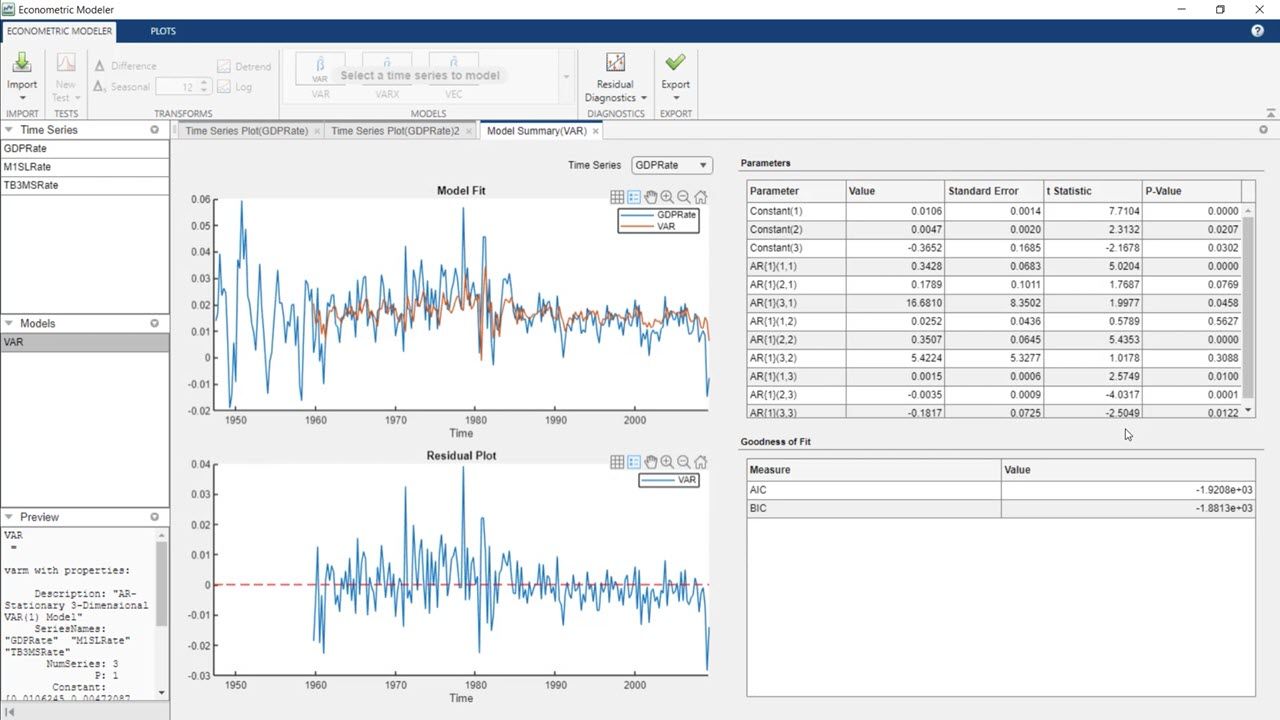

Utilisez l'application Econometric Modeler pour prétraiter, visualiser et réaliser l'identification du modèle et les estimations des paramètres. Estimez et comparez des modèles de séries temporelles univariées ou multivariées et générez du code MATLAB ou des rapports à partir de l'application.

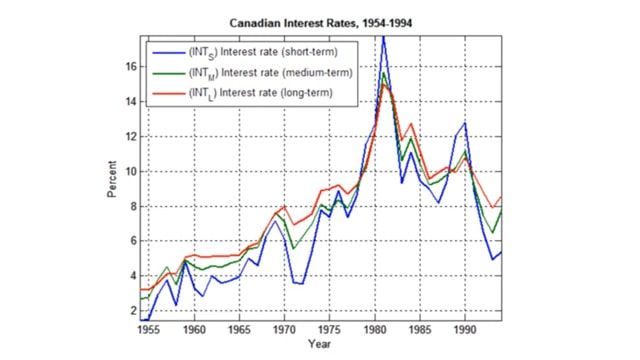

Ajustez, simulez et prévoyez des séries temporelles univariées et multivariées à l'aide de modèles ARIMA, de régression bayésienne, de type vectoriel autorégressif (VAR) et de type vectoriel à correction d'erreurs (VEC).

Ajustez, simulez et prévoyez la volatilité avec des modèles de variance de GARCH, GJR et EGARCH.

Modélisez le comportement dynamique de séries temporelles univariées et multivariées en présence de ruptures structurelles et de changements de régime économique.

.")

Créez et simulez des modèles de représentation d'état variable ou non dans le temps. Évaluez les paramètres du modèle à partir de jeux de données complets ou comportant des données manquantes avec un filtre de Kalman.

Effectuez une variété de tests de diagnostic avant et après l’estimation, tels que la stationnarité, la corrélation, l'hétéroscédasticité, le changement structurel, la colinéarité et la cointégration.

« Je suis expert en finance, et non en programmation. Pour effectuer des analyses sophistiquées sur de grandes quantités de données, j'avais besoin d'un logiciel facile à utiliser et proposant les nombreuses fonctions dont j'avais besoin. Avec MATLAB, je peux tout faire dans un seul environnement, et c'est un vrai avantage ».

Omid Rezania, CalPERS

Profitez de 30 jours pour tester.

Découvrez les tarifs et les produits.

Votre établissement propose peut-être déjà un accès à MATLAB, Simulink et d'autres produits complémentaires via la licence Campus-Wide.

Vous pouvez également sélectionner un site web dans la liste suivante :

Amériques

Europe

Asie-Pacifique