Check Fit of Multiplicative ARIMA Model

This example shows how to do goodness of fit checks. Residual diagnostic plots help verify model assumptions, and cross-validation prediction checks help assess predictive performance. The time series is monthly international airline passenger numbers from 1949 to 1960.

Load the data and estimate a model.

Load the airline data set.

load Data_Airline y = log(Data); T = length(y); Mdl = arima('Constant',0,'D',1,'Seasonality',12,... 'MALags',1,'SMALags',12); EstMdl = estimate(Mdl,y);

ARIMA(0,1,1) Model Seasonally Integrated with Seasonal MA(12) (Gaussian Distribution):

Value StandardError TStatistic PValue

_________ _____________ __________ __________

Constant 0 0 NaN NaN

MA{1} -0.37716 0.066794 -5.6466 1.6364e-08

SMA{12} -0.57238 0.085439 -6.6992 2.0952e-11

Variance 0.0012634 0.00012395 10.193 2.1406e-24

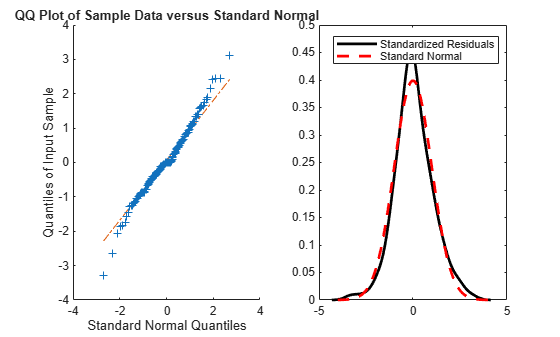

Check the residuals for normality.

One assumption of the fitted model is that the innovations follow a Gaussian distribution. Infer the residuals, and check them for normality.

res = infer(EstMdl,y); stres = res/sqrt(EstMdl.Variance); figure subplot(1,2,1) qqplot(stres) x = -4:.05:4; [f,xi] = ksdensity(stres); subplot(1,2,2) plot(xi,f,'k','LineWidth',2); hold on plot(x,normpdf(x),'r--','LineWidth',2) legend('Standardized Residuals','Standard Normal') hold off

The quantile-quantile plot (QQ-plot) and kernel density estimate show no obvious violations of the normality assumption.

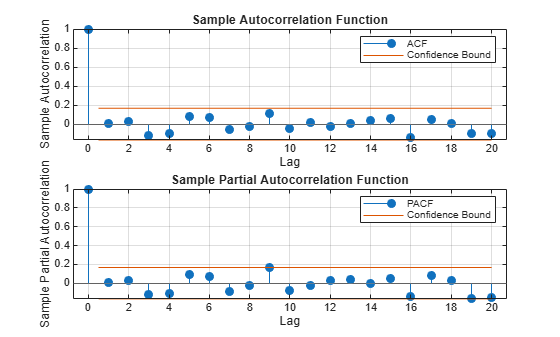

Check the residuals for autocorrelation.

Confirm that the residuals are uncorrelated. Look at the sample autocorrelation function (ACF) and partial autocorrelation function (PACF) plots for the standardized residuals.

figure subplot(2,1,1) autocorr(stres) subplot(2,1,2) parcorr(stres)

[h,p] = lbqtest(stres,'lags',[5,10,15],'dof',[3,8,13])

h = 1×3 logical array

0 0 0

p = 1×3

0.1842 0.3835 0.7321

The sample ACF and PACF plots show no significant autocorrelation. More formally, conduct a Ljung-Box Q-test at lags 5, 10, and 15, with degrees of freedom 3, 8, and 13, respectively. The degrees of freedom account for the two estimated moving average coefficients.

The Ljung-Box Q-test confirms the sample ACF and PACF results. The null hypothesis that all autocorrelations are jointly equal to zero up to the tested lag is not rejected (h = 0) for any of the three lags.

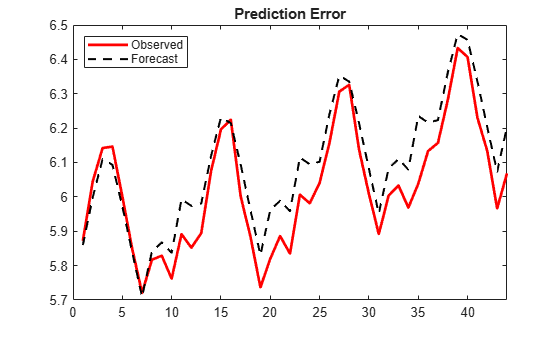

Check predictive performance.

Use a holdout sample to compute the predictive MSE of the model. Use the first 100 observations to estimate the model, and then forecast the next 44 periods.

y1 = y(1:100); y2 = y(101:end); Mdl1 = estimate(Mdl,y1);

ARIMA(0,1,1) Model Seasonally Integrated with Seasonal MA(12) (Gaussian Distribution):

Value StandardError TStatistic PValue

_________ _____________ __________ __________

Constant 0 0 NaN NaN

MA{1} -0.35674 0.089461 -3.9876 6.6739e-05

SMA{12} -0.63319 0.098744 -6.4124 1.4326e-10

Variance 0.0013285 0.00015882 8.365 6.013e-17

yF1 = forecast(Mdl1,44,'Y0',y1);

pmse = mean((y2-yF1).^2)pmse = 0.0069

figure plot(y2,'r','LineWidth',2) hold on plot(yF1,'k--','LineWidth',1.5) xlim([0,44]) title('Prediction Error') legend('Observed','Forecast','Location','northwest') hold off

The predictive ability of the model is quite good. You can optionally compare the PMSE for this model with the PMSE for a competing model to help with model selection.

See Also

Objects

Functions

Topics

- Create Seasonal ARIMA (SARIMA) Model for Time Series Data

- Estimate Seasonal ARIMA (SARIMA) Model

- Simulate Seasonal ARIMA (SARIMA) Models

- Forecast Multiplicative ARIMA Model

- Detect Autocorrelation

- Goodness of Fit

- Residual Diagnostics

- Assess Predictive Performance

- Forecast Conditional Mean Model Programmatically

- Autocorrelation and Partial Autocorrelation