Forecast VAR Model Using Monte Carlo Simulation

This example shows how to use Monte Carlo simulation via simulate to forecast a VAR model.

simulate enables you to generate simulations of time series based on your model. If you have a trustworthy VAR model object, you can use these simulations as sample forecasts.

simulate requires:

A model (

EstMdlin what follows)The number of periods for the forecast (

numobsin what follows)

simulate optionally takes:

An exogenous data series

A presample time series (

Y(end-3:end,:)in what follows)Future sample responses for conditional simulation

The number of realizations, or paths, to simulate (

2000in what follows)

Load the Data_USEconModel data set. This example uses two time series: the logarithm of real GDP, and the real 3-month T-bill rate, both differenced to be approximately stationary. For illustration, a VAR(4) model describes the time series.

load Data_USEconModel DEF = log(DataTimeTable.CPIAUCSL); GDP = log(DataTimeTable.GDP); rGDP = diff(GDP - DEF); % Real GDP is GDP - deflation TB3 = 0.01*DataTimeTable.TB3MS; dDEF = 4*diff(DEF); % Scaling rTB3 = TB3(2:end) - dDEF; % Real interest is deflated Y = [rGDP,rTB3];

Fit a VAR(4) model specification.

Mdl = varm(2,4);

Mdl.SeriesNames = {'Transformed real GDP','Transformed real 3-mo T-bill rate'};

EstMdl = estimate(Mdl,Y);Define the forecast horizon.

numobs = 21; FDates = dateshift(DataTimeTable.Time(end),'end','quarter',1:numobs);

Simulate the model for numobs steps ahead, and generate 2000 paths. Specify presample observations from the end of the data.

rng(1); %For reproducibility Ysim = simulate(EstMdl,numobs,'Y0',Y(end-3:end,:),'NumPaths',2000);

Calculate the mean and standard deviation of the simulated series:

Ymean = mean(Ysim,3); % Calculate means Ystd = std(Ysim,0,3); % Calculate std deviations

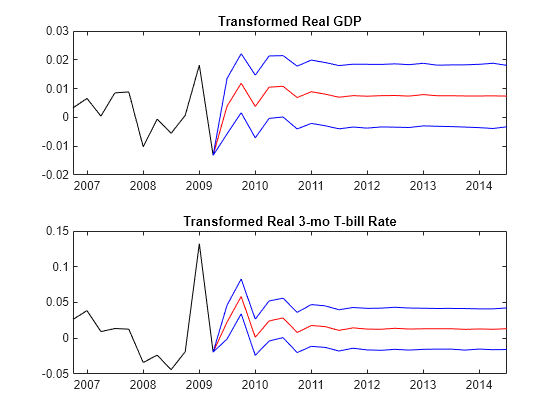

Plot the means +/- 1 standard deviation for the simulated series:

figure; subplot(2,1,1) plot(DataTimeTable.Time(end-10:end),Y(end-10:end,1),'k') hold('on') plot([DataTimeTable.Time(end) FDates],[Y(end,1);Ymean(:,1)],'r') plot([DataTimeTable.Time(end) FDates],[Y(end,1);Ymean(:,1)]+[0;Ystd(:,1)],'b') plot([DataTimeTable.Time(end) FDates],[Y(end,1);Ymean(:,1)]-[0;Ystd(:,1)],'b') title('Transformed Real GDP') subplot(2,1,2) plot(DataTimeTable.Time(end-10:end),Y(end-10:end,2),'k') hold('on') plot([DataTimeTable.Time(end) FDates],[Y(end,2);Ymean(:,2)],'r') plot([DataTimeTable.Time(end) FDates],[Y(end,2);Ymean(:,2)]+[0;Ystd(:,2)],'b') plot([DataTimeTable.Time(end) FDates],[Y(end,2);Ymean(:,2)]-[0;Ystd(:,2)],'b') title('Transformed Real 3-mo T-bill Rate')