abs2active

Convert constraints from absolute to active format

Description

ActiveConSet = abs2active(AbsConSet,Index)

Examples

Set up constraints for a portfolio optimization for portfolio w0 with constraints in the form A*w <= b, where w is absolute portfolio weights. (Absolute weights do not depend on the tracking portfolio.) Use abs2active to convert constraints in terms of absolute weights into constraints in terms of active portfolio weights, defined relative to the tracking portfolio w0. Assume three assets with the following mean and covariance of asset returns:

m = [ 0.14; 0.10; 0.05 ];

C = [ 0.29^2 0.4*0.29*0.17 0.1*0.29*0.08; 0.4*0.29*0.17 0.17^2 0.3*0.17*0.08;...

0.1*0.29*0.08 0.3*0.17*0.08 0.08^2 ];Absolute portfolio constraints are the typical ones (weights sum to 1 and fall from 0 through 1), create the A and b matrices using portcons.

AbsCons = portcons('PortValue',1,3,'AssetLims', [0; 0; 0], [1; 1; 1;]);

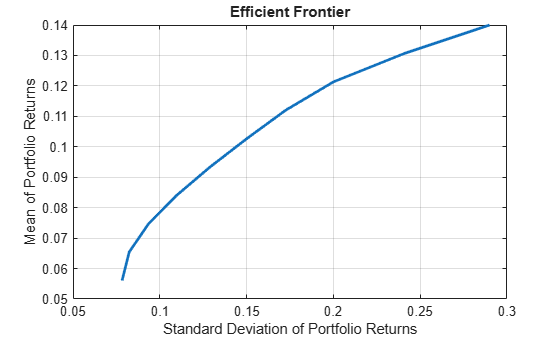

Use the Portfolio object to determine the efficient frontier.

p = Portfolio('AssetMean', m, 'AssetCovar', C); p = p.setInequality(AbsCons(:,1:end-1), AbsCons(:,end)); p.plotFrontier;

The tracking portfolio w0 is:

w0 = [ 0.1; 0.55; 0.35 ];

Use abs2active to compute the constraints for active portfolio weights.

ActCons = abs2active(AbsCons, w0)

ActCons = 8×4

1.0000 1.0000 1.0000 0

-1.0000 -1.0000 -1.0000 0

1.0000 0 0 0.9000

0 1.0000 0 0.4500

0 0 1.0000 0.6500

-1.0000 0 0 0.1000

0 -1.0000 0 0.5500

0 0 -1.0000 0.3500

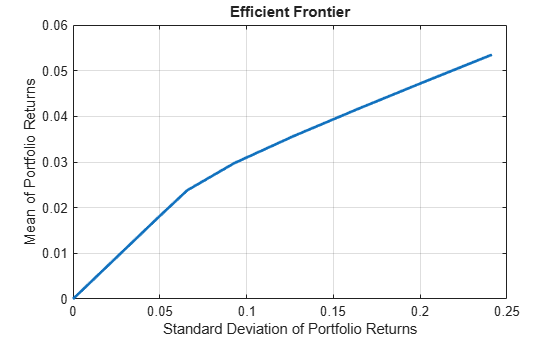

Use the Portfolio object p and its efficient frontier to demonstrate expected returns and risk relative to the tracking portfolio w0.

p = p.setInequality(ActCons(:,1:end-1), ActCons(:,end)); p.plotFrontier;

Note, when using abs2active to compute “active constraints” for use with a Portfolio object, don't use the Portfolio object’s default constraints because the relative weights can be positive or negative (the setDefaultConstraints function for a Portfolio object specifies weights to be nonnegative).

Input Arguments

Output Arguments

Algorithms

abs2active transforms a constraint matrix to an equivalent matrix

expressed in active weight format (relative to the index). The transformation equation

is

Therefore

The initial constraint matrix consists of

NCONSTRAINTS portfolio linear inequality constraints expressed in

absolute weight format. The index portfolio vector contains NASSETS

assets.

Version History

Introduced before R2006a

See Also

active2abs | pcalims | pcglims | pcpval | portcons | Portfolio | setInequality