swapbyzero

Price swap instrument from set of zero curves and price cross-currency swaps

Syntax

Description

[

prices a swap instrument. You can use Price,SwapRate,AI,RecCF,RecCFDates,PayCF,PayCFDates]

= swapbyzero(RateSpec,LegRate,Settle,Maturity)swapbyzero to compute prices of

vanilla swaps, amortizing swaps, and forward swaps. All inputs are either scalars or

NINST-by-1 vectors unless otherwise specified. Any

date can be a date character vector. An optional argument can be passed as an empty matrix

[].

Note

Alternatively, you can use the Swap object to price swap

instruments and the CurrencySwap object

to price cross-currency swap instruments. For more information, see Get Started with Workflows Using Object-Based Framework for Pricing Financial Instruments.

[ prices

a swap instrument with additional options specified by one or more Price,SwapRate,AI,RecCF,RecCFDates,PayCF,PayCFDates]

= swapbyzero(RateSpec,LegRate,Settle,Maturity,Name,Value)Name,Value pair

arguments. You can use swapbyzero to compute prices

of vanilla swaps, amortizing swaps, forward swaps, and cross-currency

swaps. For more information on the name-value pairs for vanilla swaps,

amortizing swaps, and forward swaps, see Vanilla

Swaps, Amortizing Swaps, Forward Swaps.

Specifically, you can use name-value pairs for FXRate, ExchangeInitialPrincipal,

and ExchangeMaturityPrincipal to compute the

price for cross-currency swaps. For more information on the name-value

pairs for cross-currency swaps, see Cross-Currency

Swaps.

Examples

Price an interest-rate swap with a fixed receiving leg and a floating paying leg. Payments are made once a year, and the notional principal amount is $100. The values for the remaining arguments are:

Coupon rate for fixed leg: 0.06 (6%)

Spread for floating leg: 20 basis points

Swap settlement date: Jan. 01, 2000

Swap maturity date: Jan. 01, 2003

Based on the information above, set the required arguments and build the LegRate, LegType, and LegReset matrices:

Settle = datetime(2000,1,1); Maturity = datetime(2003,1,1); Basis = 0; Principal = 100; LegRate = [0.06 20]; % [CouponRate Spread] LegType = [1 0]; % [Fixed Float] LegReset = [1 1]; % Payments once per year

Load the file deriv.mat, which provides ZeroRateSpec, the interest-rate term structure needed to price the bond.

load deriv.mat;Use swapbyzero to compute the price of the swap.

Price = swapbyzero(ZeroRateSpec, LegRate, Settle, Maturity,... LegReset, Basis, Principal, LegType)

Price = 3.6923

Using the previous data, calculate the swap rate, which is the coupon rate for the fixed leg, such that the swap price at time = 0 is zero.

LegRate = [NaN 20];

[Price, SwapRate] = swapbyzero(ZeroRateSpec, LegRate, Settle,...

Maturity, LegReset, Basis, Principal, LegType)Price = 0

SwapRate = 0.0466

In swapbyzero , if Settle is not on a reset date (and 'StartDate' is not specified), the effective date is assumed to be the previous reset date before Settle in order to compute the accrued interest and dirty price. In this example, the effective date is ( '15-Sep-2009' ), which is the previous reset date before the ( '08-Jun-2010' ) Settle date.

Use swapbyzero with name-value pair arguments for LegRate, LegType, LatestFloatingRate, AdjustCashFlowsBasis, and BusinessDayConvention to calculate output for Price, SwapRate, AI, RecCF, RecCFDates, PayCF, and PayCFDates:

Settle = datetime(2008,6,1); RateSpec = intenvset('Rates', [.005 .0075 .01 .014 .02 .025 .03]',... 'StartDates',Settle, 'EndDates',[datetime(2010,12,8) , datetime(2011,6,8) , datetime(2012,6,8) , datetime(2013,6,8) , datetime(2015,6,8) , datetime(2017,6,8) ,datetime(2020,6,8)]'); Maturity = datetime(2020,9,15); LegRate = [.025 50]; LegType = [1 0]; % fixed/floating LatestFloatingRate = .005; [Price, SwapRate, AI, RecCF, RecCFDates, PayCF,PayCFDates] = ... swapbyzero(RateSpec, LegRate, Settle, Maturity,'LegType',LegType,... 'LatestFloatingRate',LatestFloatingRate,'AdjustCashFlowsBasis',true,... 'BusinessDayConvention','modifiedfollow')

Price = -7.7485

SwapRate = NaN

AI = 1.4098

RecCF = 1×14

-1.7623 2.4863 2.5000 2.5000 2.5000 2.5137 2.4932 2.4932 2.5000 2.5000 2.5000 2.5137 2.4932 102.4932

RecCFDates = 1×14

733560 733666 734031 734396 734761 735129 735493 735857 736222 736588 736953 737320 737684 738049

PayCF = 1×14

-0.3525 0.4973 1.0006 1.0006 2.0510 2.5944 3.6040 3.8939 4.4152 4.6923 4.9895 4.8400 5.1407 104.9126

PayCFDates = 1×14

733560 733666 734031 734396 734761 735129 735493 735857 736222 736588 736953 737320 737684 738049

Price three swaps using two interest-rate curves. First, define the data for the interest-rate term structure:

StartDates = datetime(2012,5,1); EndDates = [datetime(2013,5,1) ; datetime(2014,5,1) ; datetime(2015,5,1) ; datetime(2016,5,1)]; Rates = [[0.0356;0.041185;0.04489;0.047741],[0.0366;0.04218;0.04589;0.04974]];

Create the RateSpec using intenvset.

RateSpec = intenvset('Rates', Rates, 'StartDates',StartDates,... 'EndDates', EndDates, 'Compounding', 1)

RateSpec = struct with fields:

FinObj: 'RateSpec'

Compounding: 1

Disc: [4×2 double]

Rates: [4×2 double]

EndTimes: [4×1 double]

StartTimes: [4×1 double]

EndDates: [4×1 double]

StartDates: 734990

ValuationDate: 734990

Basis: 0

EndMonthRule: 1

Look at the Rates for the two interest-rate curves.

RateSpec.Rates

ans = 4×2

0.0356 0.0366

0.0412 0.0422

0.0449 0.0459

0.0477 0.0497

Define the swap instruments.

Settle = datetime(2012,5,1);

Maturity = datetime(2015,5,1);

LegRate = [0.06 10];

Principal = [100;50;100]; % Three notional amountsPrice three swaps using two curves.

Price = swapbyzero(RateSpec, LegRate, Settle, Maturity, 'Principal', Principal)Price = 3×2

3.9688 3.6869

1.9844 1.8434

3.9688 3.6869

Price a swap using two interest-rate curves. First, define data for the two interest-rate term structures:

StartDates = datetime(2012,5,1); EndDates = [datetime(2013,5,1) ; datetime(2014,5,1) ; datetime(2015,5,1) ; datetime(2016,5,1)]; Rates1 = [0.0356;0.041185;0.04489;0.047741]; Rates2 = [0.0366;0.04218;0.04589;0.04974];

Create the RateSpec using intenvset.

RateSpecReceiving = intenvset('Rates', Rates1, 'StartDates',StartDates,... 'EndDates', EndDates, 'Compounding', 1); RateSpecPaying= intenvset('Rates', Rates2, 'StartDates',StartDates,... 'EndDates', EndDates, 'Compounding', 1); RateSpec=[RateSpecReceiving RateSpecPaying]

RateSpec=1×2 struct array with fields:

FinObj

Compounding

Disc

Rates

EndTimes

StartTimes

EndDates

StartDates

ValuationDate

Basis

EndMonthRule

Define the swap instruments.

Settle = datetime(2012,5,1); Maturity = datetime(2015,5,1); LegRate = [0.06 10]; Principal = [100;50;100];

Price three swaps using the two curves.

Price = swapbyzero(RateSpec, LegRate, Settle, Maturity, 'Principal', Principal)Price = 3×1

3.9693

1.9846

3.9693

To compute a forward par swap rate, set the StartDate parameter to a future date and set the fixed coupon rate in the LegRate input to NaN.

Define the zero curve data and build a zero curve using IRDataCurve.

ZeroRates = [2.09 2.47 2.71 3.12 3.43 3.85 4.57]'/100; Settle = datetime(2012,1,1); EndDates = datemnth(Settle,12*[1 2 3 5 7 10 20]'); Compounding = 1; ZeroCurve = IRDataCurve('Zero',Settle,EndDates,ZeroRates,'Compounding',Compounding)

ZeroCurve = Type: Zero Settle: 734869 (01-Jan-2012) Compounding: 1 Basis: 0 (actual/actual) InterpMethod: linear Dates: [7x1 double] Data: [7x1 double]

Create a RateSpec structure using the toRateSpec method.

RateSpec = ZeroCurve.toRateSpec(EndDates)

RateSpec = struct with fields:

FinObj: 'RateSpec'

Compounding: 1

Disc: [7×1 double]

Rates: [7×1 double]

EndTimes: [7×1 double]

StartTimes: [7×1 double]

EndDates: [7×1 double]

StartDates: 734869

ValuationDate: 734869

Basis: 0

EndMonthRule: 1

Compute the forward swap rate (the coupon rate for the fixed leg), such that the forward swap price at time = 0 is zero. The forward swap starts in a month (1-Feb-2012) and matures in 10 years (1-Feb-2022).

StartDate = datetime(2012,2,1); Maturity = datetime(2022,2,1); LegRate = [NaN 0]; [Price, SwapRate] = swapbyzero(RateSpec, LegRate, Settle, Maturity,... 'StartDate', StartDate)

Price = 0

SwapRate = 0.0378

The swapbyzero function generates the cash flow dates based on the Settle and Maturity dates, while using the Maturity date as the "anchor" date from which to count backwards in regular intervals. By default, swapbyzero does not distinguish non-business days from business days. To make swapbyzero move non-business days to the following business days, you can you can set the optional name-value input argument BusinessDayConvention with a value of follow.

Define the zero curve data and build a zero curve using IRDataCurve.

ZeroRates = [2.09 2.47 2.71 3.12 3.43 3.85 4.57]'/100; Settle = datetime(2012,1,5); EndDates = datemnth(Settle,12*[1 2 3 5 7 10 20]'); Compounding = 1; ZeroCurve = IRDataCurve('Zero',Settle,EndDates,ZeroRates,'Compounding',Compounding); RateSpec = ZeroCurve.toRateSpec(EndDates); StartDate = datetime(2012,2,5); Maturity = datetime(2022,2,5); LegRate = [NaN 0];

To demonstrate the optional input BusinessDayConvention, swapbyzero is first used without and then with the optional name-value input argument BusinessDayConvention. Notice that when using BusinessDayConvention, all days are business days.

[Price1,SwapRate1,~,~,RecCFDates1,~,PayCFDates1] = swapbyzero(RateSpec,LegRate,Settle,Maturity,... 'StartDate',StartDate); datestr(RecCFDates1)

ans = 11×11 char array

'05-Jan-2012'

'05-Feb-2013'

'05-Feb-2014'

'05-Feb-2015'

'05-Feb-2016'

'05-Feb-2017'

'05-Feb-2018'

'05-Feb-2019'

'05-Feb-2020'

'05-Feb-2021'

'05-Feb-2022'

isbusday(RecCFDates1)

ans = 11×1 logical array

1

1

1

1

1

0

1

1

1

1

0

[Price2,SwapRate2,~,~,RecCFDates2,~,PayCFDates2] = swapbyzero(RateSpec,LegRate,Settle,Maturity,... 'StartDate',StartDate,'BusinessDayConvention','follow'); datestr(RecCFDates2)

ans = 12×11 char array

'05-Jan-2012'

'06-Feb-2012'

'05-Feb-2013'

'05-Feb-2014'

'05-Feb-2015'

'05-Feb-2016'

'06-Feb-2017'

'05-Feb-2018'

'05-Feb-2019'

'05-Feb-2020'

'05-Feb-2021'

'07-Feb-2022'

isbusday(RecCFDates2)

ans = 12×1 logical array

1

1

1

1

1

1

1

1

1

1

1

1

Price an amortizing swap using the Principal input argument to define the amortization schedule.

Create the RateSpec.

Rates = 0.035; ValuationDate = datetime(2011,1,1); StartDates = ValuationDate; EndDates = datetime(2017,1,1); Compounding = 1; RateSpec = intenvset('ValuationDate', ValuationDate,'StartDates', StartDates,... 'EndDates', EndDates,'Rates', Rates, 'Compounding', Compounding);

Create the swap instrument using the following data:

Settle = datetime(2011,1,1); Maturity = datetime(2017,1,1); LegRate = [0.04 10];

Define the swap amortizing schedule.

Principal ={{datetime(2013,1,1) 100;datetime(2014,1,1) 80;datetime(2015,1,1) 60;datetime(2016,1,1) 40;datetime(2017,1,1) 20}};Compute the price of the amortizing swap.

Price = swapbyzero(RateSpec, LegRate, Settle, Maturity, 'Principal' , Principal)Price = 1.4574

Price a forward swap using the StartDate input argument to define the future starting date of the swap.

Create the RateSpec.

Rates = 0.0325; ValuationDate = datetime(2012,1,1); StartDates = ValuationDate; EndDates = datetime(2018,1,1); Compounding = 1; RateSpec = intenvset('ValuationDate', ValuationDate,'StartDates', StartDates,... 'EndDates', EndDates,'Rates', Rates, 'Compounding', Compounding)

RateSpec = struct with fields:

FinObj: 'RateSpec'

Compounding: 1

Disc: 0.8254

Rates: 0.0325

EndTimes: 6

StartTimes: 0

EndDates: 737061

StartDates: 734869

ValuationDate: 734869

Basis: 0

EndMonthRule: 1

Compute the price of a forward swap that starts in a year (Jan 1, 2013) and matures in three years with a forward swap rate of 4.27%.

Settle = datetime(2012,1,1);

StartDate = datetime(2013,1,1);

Maturity = datetime(2016,1,1);

LegRate = [0.0427 10];

Price = swapbyzero(RateSpec, LegRate, Settle, Maturity, 'StartDate' , StartDate)Price = 2.5083

Using the previous data, compute the forward swap rate, the coupon rate for the fixed leg, such that the forward swap price at time = 0 is zero.

LegRate = [NaN 10]; [Price, SwapRate] = swapbyzero(RateSpec, LegRate, Settle, Maturity,... 'StartDate' , StartDate)

Price = 0

SwapRate = 0.0335

If Settle is not on a reset

date of a floating-rate note, swapbyzero attempts

to obtain the latest floating rate before Settle from RateSpec or

the LatestFloatingRate parameter. When the reset

date for this rate is out of the range of RateSpec (and LatestFloatingRate is

not specified), swapbyzero fails to obtain the

rate for that date and generates an error. This example shows how

to use the LatestFloatingRate input parameter to

avoid the error.

Create the error condition when a swap instrument’s StartDate cannot

be determined from the RateSpec.

Settle = datetime(2000,1,1); Maturity = datetime(2003,12,1); Basis = 0; Principal = 100; LegRate = [0.06 20]; % [CouponRate Spread] LegType = [1 0]; % [Fixed Float] LegReset = [1 1]; % Payments once per year load deriv.mat; Price = swapbyzero(ZeroRateSpec,LegRate,Settle,Maturity,... 'LegReset',LegReset,'Basis',Basis,'Principal',Principal, ... 'LegType',LegType)

Error using floatbyzero (line 256) The rate at the instrument starting date cannot be obtained from RateSpec. Its reset date (01-Dec-1999) is out of the range of dates contained in RateSpec. This rate is required to calculate cash flows at the instrument starting date. Consider specifying this rate with the 'LatestFloatingRate' input parameter. Error in swapbyzero (line 289) [FloatFullPrice, FloatPrice,FloatCF,FloatCFDates] = floatbyzero(FloatRateSpec, Spreads, Settle,...

Here, the reset date for the rate at Settle was 01-Dec-1999,

which was earlier than the valuation date of ZeroRateSpec (01-Jan-2000).

This error can be avoided by specifying the rate at the swap instrument’s

starting date using the LatestFloatingRate input

parameter.

Define LatestFloatingRate and calculate

the floating-rate price.

Price = swapbyzero(ZeroRateSpec,LegRate,Settle,Maturity,... 'LegReset',LegReset,'Basis',Basis,'Principal',Principal, ... 'LegType',LegType,'LatestFloatingRate',0.03)

Price =

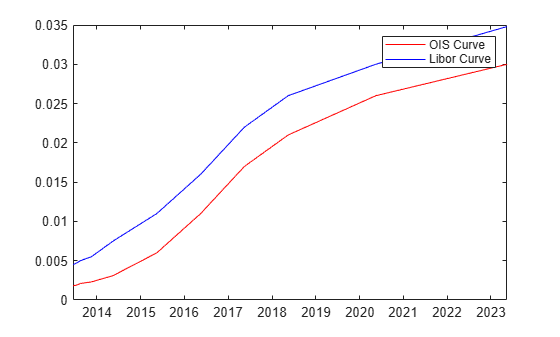

4.7594Define the OIS and Libor rates.

Settle = datetime(2013,5,15); CurveDates = daysadd(Settle,360*[1/12 2/12 3/12 6/12 1 2 3 4 5 7 10],1); OISRates = [.0018 .0019 .0021 .0023 .0031 .006 .011 .017 .021 .026 .03]'; LiborRates = [.0045 .0047 .005 .0055 .0075 .011 .016 .022 .026 .030 .0348]';

Plot the dual curves.

figure,plot(CurveDates,OISRates,'r');hold on;plot(CurveDates,LiborRates,'b') legend({'OIS Curve', 'Libor Curve'})

Create an associated RateSpec for the OIS and Libor curves.

OISCurve = intenvset('Rates',OISRates,'StartDate',Settle,'EndDates',CurveDates); LiborCurve = intenvset('Rates',LiborRates,'StartDate',Settle,'EndDates',CurveDates);

Define the swap.

Maturity = datetime(2018,5,15); % Five year swap

FloatSpread = 0;

FixedRate = .025;

LegRate = [FixedRate FloatSpread];Compute the price of the swap instrument. The LiborCurve term structure will be used to generate the cash flows of the floating leg. The OISCurve term structure will be used for discounting the cash flows.

Price = swapbyzero(OISCurve, LegRate, Settle,... Maturity,'ProjectionCurve',LiborCurve)

Price = -0.3697

Compare results when the term structure OISCurve is used both for discounting and also generating the cash flows of the floating leg.

PriceSwap = swapbyzero(OISCurve, LegRate, Settle, Maturity)

PriceSwap = 2.0517

Price an existing cross currency swap that receives a fixed rate of JPY and pays a fixed rate of USD at an annual frequency.

Settle = datetime(2015,8,15); Maturity = datetime(2018,8,15); Reset = 1; LegType = [1 1]; % Fixed-Fixed r_USD = .09; r_JPY = .04; FixedRate_USD = .08; FixedRate_JPY = .05; Principal_USD = 10000000; Principal_JPY = 1200000000; S = 1/110; RateSpec_USD = intenvset('StartDate',Settle,'EndDate', Maturity,'Rates',r_USD,'Compounding',-1); RateSpec_JPY = intenvset('StartDate',Settle,'EndDate', Maturity,'Rates', r_JPY,'Compounding',-1); Price = swapbyzero([RateSpec_JPY RateSpec_USD], [FixedRate_JPY FixedRate_USD],... Settle, Maturity,'Principal',[Principal_JPY Principal_USD],'FXRate',[S 1], 'LegType',LegType)

Price = 1.5430e+06

Price a new swap where you pay a EUR float and receive a USD float.

Settle = datetime(2015,12,22); Maturity = datetime(2018,8,15); LegRate = [0 -50/10000]; LegType = [0 0]; % Float Float LegReset = [4 4]; FXRate = 1.1; Notional = [10000000 8000000]; USD_Dates = datemnth(Settle,[1 3 6 12*[1 2 3 5 7 10 20 30]]'); USD_Zero = [0.03 0.06 0.08 0.13 0.36 0.76 1.63 2.29 2.88 3.64 3.89]'/100; Curve_USD = intenvset('StartDate',Settle,'EndDates',USD_Dates,'Rates',USD_Zero); EUR_Dates = datemnth(Settle,[3 6 12*[1 2 3 5 7 10 20 30]]'); EUR_Zero = [0.017 0.033 0.088 .27 .512 1.056 1.573 2.183 2.898 2.797]'/100; Curve_EUR = intenvset('StartDate',Settle,'EndDates',EUR_Dates,'Rates',EUR_Zero); Price = swapbyzero([Curve_USD Curve_EUR], ... LegRate, Settle, Maturity,'LegType',LegType,'LegReset',LegReset,'Principal',Notional,... 'FXRate',[1 FXRate],'ExchangeInitialPrincipal',false)

Price = 1.2002e+06

Input Arguments

Name-Value Arguments

Output Arguments

More About

References

[1] Hull, J. Options, Futures and Other Derivatives Fourth Edition. Prentice Hall, 2000.

Version History

Introduced before R2006aSee Also

bondbyzero | intenvset | cfbyzero | fixedbyzero | floatbyzero | Swap