lagmatrix

Create lagged time series data

Syntax

Description

LagTbl = lagmatrix(Tbl,lags)DataVariables name-value argument. (since R2022a)

[___] = lagmatrix(___,

specifies options using one or more name-value arguments in

addition to any of the input argument combinations in previous syntaxes.

Name=Value)lagmatrix returns the output argument combination for the

corresponding input arguments. For example,

lagmatrix(Tbl,1,Y0=zeros(1,5),DataVariables=1:5) lags, by one period,

the first five variables in the input table Tbl and sets the presample

of each series to 0.

Examples

Input Arguments

Name-Value Arguments

Specify optional pairs of arguments as

Name1=Value1,...,NameN=ValueN, where Name is

the argument name and Value is the corresponding value.

Name-value arguments must appear after other arguments, but the order of the

pairs does not matter.

Before R2021a, use commas to separate each name and value, and enclose

Name in quotes.

Example: lagmatrix(Tbl,1,Y0=zeros(1,5),DataVariables=1:5) lags, by one

period, the first 5 variables in the input table Tbl and sets the

presample of each series to 0.

Since R2022a

Presample data to backward fill lagged series, specified as a matrix with

numVars columns, or a table or timetable. For a table or

timetable, the DataVariables name-value argument selects the

variables in Y0 to shift.

Y0 must have the same data type as the input data.

Timetables must have regular sample times preceding times in

Tbl.

lagmatrix fills required presample values from the end of

Y0.

Example: Y0=zeros(size(Y,2),2)

Since R2022a

Postsample data to frontward fill led series, specified as a matrix with

numVars columns, or a table or timetable. For a table or

timetable, the DataVariables name-value argument selects the

variables in YF to shift. The default for postsample data is

NaN.

YF must have the same data type as the input data.

Timetables must have regular sample times following times in

Tbl.

lagmatrix fills required postsample values from the

beginning of YF.

Example: YF=ones(size(Y,2),3)

Since R2022a

Variables in Tbl, Y0, and

YF, from which lagmatrix creates shifted

time series data, specified as a string vector or cell vector of character vectors

containing variable names in Tbl.Properties.VariableNames, or an

integer or logical vector representing the indices of names. The selected variables

must be numeric.

Example: DataVariables=["GDP" "CPI"]

Example: DataVariables=[true true false false] or

DataVariables=[1 2] selects the first and second table

variables.

Data Types: double | logical | char | cell | string

Since R2022a

Part of the shifted series to appear in the outputs, specified as a value in this table.

| Value | Description |

|---|---|

"full" | Outputs contain all values in the input time series data and all

specified presample Y0 or postsample

Yf values on an expanded time base. |

"same" | Outputs contain only values on the original time base. |

"valid" | Outputs contain values for times at which all series have specified

(non-NaN) values. |

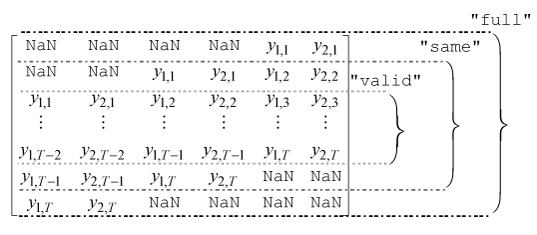

To illustrate the shape of the output shifted time series for each

value of Shape, suppose the input time series data is a 2-D

series with numObs = T observations and lags is [1 0 -1]. The

output shifted series is one of the three T-by-6 matrix arrays in

this figure.

Example: Shape="full"

Data Types: char | string