Bias Mitigation in Credit Scoring by Disparate Impact Removal

Disparate impact removal is a pre-processing technique in bias mitigation. Using this technique, you modify the original credit score data to increase group fairness, while still preserving rank ordering within groups. Using a disparate impact removal technique reduces the bias introduced by the credit scoring model more than if you use the original data to train the credit scoring model. You perform the disparate impact removal technique using the disparateImpactRemover class from the Statistics and Machine Learning Toolbox™. This class returns a remover object along with a table containing the new predictor values. However, you need to use the transform method with the remover object on the test data before you can predict using the fitted credit scoring model.

The disparate impact removal technique works only with the distribution of data within a numeric predictor for each subgroup of a sensitive attribute. The disparateImpactRemover class has no knowledge of, or relation to, the response variable. In this example, you treat all the numeric predictors, time at address (TmAtAddress), customer income (CustIncome), time with Bank (TmWBank), average monthly balance (AMBalance), and utilization rate (UtilRate), with respect to the sensitive attribute, customer age (AgeGroup).

Original Credit Scoring Model

This example uses a credit scoring workflow. Load the CreditCardData.mat and use the 'data' data set.

load CreditCardData.mat AgeGroup = discretize(data.CustAge,[min(data.CustAge) 30 45 60 max(data.CustAge)], ... 'categorical',{'Age < 30','30 <= Age < 45','45 <= Age < 60','Age >= 60'}); data = addvars(data,AgeGroup,'After','CustAge'); head(data)

CustID CustAge AgeGroup TmAtAddress ResStatus EmpStatus CustIncome TmWBank OtherCC AMBalance UtilRate status

______ _______ ______________ ___________ __________ _________ __________ _______ _______ _________ ________ ______

1 53 45 <= Age < 60 62 Tenant Unknown 50000 55 Yes 1055.9 0.22 0

2 61 Age >= 60 22 Home Owner Employed 52000 25 Yes 1161.6 0.24 0

3 47 45 <= Age < 60 30 Tenant Employed 37000 61 No 877.23 0.29 0

4 50 45 <= Age < 60 75 Home Owner Employed 53000 20 Yes 157.37 0.08 0

5 68 Age >= 60 56 Home Owner Employed 53000 14 Yes 561.84 0.11 0

6 65 Age >= 60 13 Home Owner Employed 48000 59 Yes 968.18 0.15 0

7 34 30 <= Age < 45 32 Home Owner Unknown 32000 26 Yes 717.82 0.02 1

8 50 45 <= Age < 60 57 Other Employed 51000 33 No 3041.2 0.13 0

rng('default')Split the data set into training and testing data.

c = cvpartition(size(data,1),'HoldOut',0.3);

data_Train = data(c.training(),:);

data_Test = data(c.test(),:);

head(data_Train) CustID CustAge AgeGroup TmAtAddress ResStatus EmpStatus CustIncome TmWBank OtherCC AMBalance UtilRate status

______ _______ ______________ ___________ __________ _________ __________ _______ _______ _________ ________ ______

1 53 45 <= Age < 60 62 Tenant Unknown 50000 55 Yes 1055.9 0.22 0

2 61 Age >= 60 22 Home Owner Employed 52000 25 Yes 1161.6 0.24 0

3 47 45 <= Age < 60 30 Tenant Employed 37000 61 No 877.23 0.29 0

4 50 45 <= Age < 60 75 Home Owner Employed 53000 20 Yes 157.37 0.08 0

7 34 30 <= Age < 45 32 Home Owner Unknown 32000 26 Yes 717.82 0.02 1

8 50 45 <= Age < 60 57 Other Employed 51000 33 No 3041.2 0.13 0

9 50 45 <= Age < 60 10 Tenant Unknown 52000 25 Yes 115.56 0.02 1

10 49 45 <= Age < 60 30 Home Owner Unknown 53000 23 Yes 718.5 0.17 1

Use creditscorecard to create a creditscorecard object and use fitmodel to fit a credit scoring model with the training data (data_Train).

PredictorVars = setdiff(data_Train.Properties.VariableNames, ... {'CustAge','AgeGroup','CustID','status'}); sc1 = creditscorecard(data_Train,'IDVar','CustID', ... 'PredictorVars',PredictorVars,'ResponseVar','status'); sc1 = autobinning(sc1); sc1 = fitmodel(sc1,'VariableSelection','fullmodel');

Generalized linear regression model:

logit(status) ~ 1 + TmAtAddress + ResStatus + EmpStatus + CustIncome + TmWBank + OtherCC + AMBalance + UtilRate

Distribution = Binomial

Estimated Coefficients:

Estimate SE tStat pValue

________ ________ ________ __________

(Intercept) 0.73924 0.077237 9.5711 1.058e-21

TmAtAddress 1.2577 0.99118 1.2689 0.20448

ResStatus 1.755 1.295 1.3552 0.17535

EmpStatus 0.88652 0.32232 2.7504 0.0059516

CustIncome 0.95991 0.19645 4.8862 1.0281e-06

TmWBank 1.132 0.3157 3.5856 0.00033637

OtherCC 0.85227 2.1198 0.40204 0.68765

AMBalance 1.0773 0.31969 3.3698 0.00075232

UtilRate -0.19784 0.59565 -0.33214 0.73978

840 observations, 831 error degrees of freedom

Dispersion: 1

Chi^2-statistic vs. constant model: 66.5, p-value = 2.44e-11

Use displaypoints to compute the points per predictor per bin for the creditscorecard model (sc1).

pointsinfo1 = displaypoints(sc1)

pointsinfo1=38×3 table

Predictors Bin Points

_______________ _________________ _________

{'TmAtAddress'} {'[-Inf,9)' } -0.17538

{'TmAtAddress'} {'[9,16)' } 0.05434

{'TmAtAddress'} {'[16,23)' } 0.096897

{'TmAtAddress'} {'[23,Inf]' } 0.13984

{'TmAtAddress'} {'<missing>' } NaN

{'ResStatus' } {'Tenant' } -0.017688

{'ResStatus' } {'Home Owner' } 0.11681

{'ResStatus' } {'Other' } 0.29011

{'ResStatus' } {'<missing>' } NaN

{'EmpStatus' } {'Unknown' } -0.097582

{'EmpStatus' } {'Employed' } 0.33162

{'EmpStatus' } {'<missing>' } NaN

{'CustIncome' } {'[-Inf,30000)' } -0.61962

{'CustIncome' } {'[30000,36000)'} -0.10695

{'CustIncome' } {'[36000,40000)'} 0.0010845

{'CustIncome' } {'[40000,42000)'} 0.065532

⋮

Use probdefault to determine the likelihood of default for the data_Test data set and the creditscorecard model (sc1).

pd1 = probdefault(sc1,data_Test); threshold = 0.35; predictions1 = double(pd1>threshold);

Use fairnessMetrics to compute fairness metrics at the model level as a baseline. Use report to generate the fairness metrics report.

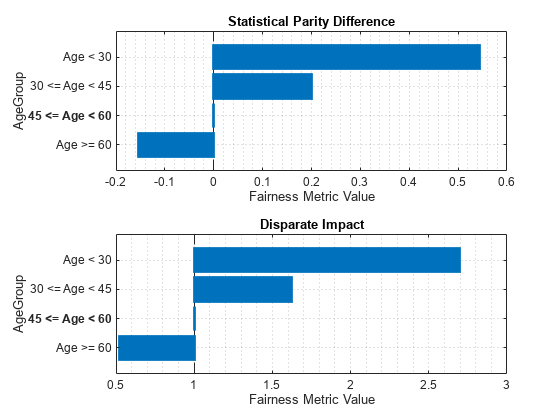

modelMetrics1 = fairnessMetrics(data_Test,'status','Predictions',predictions1,'SensitiveAttributeNames','AgeGroup'); mmReport1 = report(modelMetrics1,'GroupMetrics','GroupCount')

mmReport1=4×8 table

ModelNames SensitiveAttributeNames Groups StatisticalParityDifference DisparateImpact EqualOpportunityDifference AverageAbsoluteOddsDifference GroupCount

__________ _______________________ ______________ ___________________________ _______________ __________________________ _____________________________ __________

Model1 AgeGroup Age < 30 0.54312 2.6945 0.47391 0.5362 22

Model1 AgeGroup 30 <= Age < 45 0.19922 1.6216 0.35645 0.22138 152

Model1 AgeGroup 45 <= Age < 60 0 1 0 0 156

Model1 AgeGroup Age >= 60 -0.15385 0.52 -0.18323 0.16375 30

Use plot to visualize the statistical parity difference ('spd') and disparate impact ('di') bias metrics.

figure tiledlayout(2,1) nexttile plot(modelMetrics1,'spd') nexttile plot(modelMetrics1,'di')

Bias Mitigation by Disparate Impact Removal

For each of the five continuous predictors, 'TmAtAddress', 'CustIncome', 'TmWBank', 'AMBalance', and 'UtilRate' plot the original distributions of data within each age group.

Choose a numeric predictor to plot.

predictor ="CustIncome"; [f1, xi1] = ksdensity(data_Train.(predictor)(data_Train.AgeGroup=='Age < 30')); [f2, xi2] = ksdensity(data_Train.(predictor)(data_Train.AgeGroup=='30 <= Age < 45')); [f3, xi3] = ksdensity(data_Train.(predictor)(data_Train.AgeGroup=='45 <= Age < 60')); [f4, xi4] = ksdensity(data_Train.(predictor)(data_Train.AgeGroup=='Age >= 60'));

Create a disparateImpactRemover object and return the newTrainTbl table with the new predictor values.

[remover, newTrainTbl] = disparateImpactRemover(data_Train, 'AgeGroup' , 'PredictorNames', {'TmAtAddress','CustIncome','TmWBank','AMBalance','UtilRate'})

remover =

disparateImpactRemover with properties:

RepairFraction: 1

PredictorNames: {'TmAtAddress' 'CustIncome' 'TmWBank' 'AMBalance' 'UtilRate'}

SensitiveAttribute: 'AgeGroup'

newTrainTbl=840×12 table

CustID CustAge AgeGroup TmAtAddress ResStatus EmpStatus CustIncome TmWBank OtherCC AMBalance UtilRate status

______ _______ ______________ ___________ __________ _________ __________ _______ _______ _________ ________ ______

1 53 45 <= Age < 60 58.599 Tenant Unknown 47000 51.733 Yes 1009.4 0.20099 0

2 61 Age >= 60 24 Home Owner Employed 41500 24.5 Yes 1203.9 0.25 0

3 47 45 <= Age < 60 30.5 Tenant Employed 33500 57.686 No 817.9 0.29 0

4 50 45 <= Age < 60 68.622 Home Owner Employed 49401 19.07 Yes 120.54 0.077267 0

7 34 30 <= Age < 45 30.5 Home Owner Unknown 35500 26.657 Yes 638.88 0.02 1

8 50 45 <= Age < 60 53.39 Other Employed 47000 27.971 No 2172.7 0.12 0

9 50 45 <= Age < 60 9 Tenant Unknown 49401 22.541 Yes 120.54 0.02 1

10 49 45 <= Age < 60 30.5 Home Owner Unknown 49401 22 Yes 664.51 0.14715 1

11 52 45 <= Age < 60 24 Tenant Unknown 30500 38.779 Yes 120.54 0.065 1

12 48 45 <= Age < 60 77.291 Other Unknown 40500 14.5 Yes 405.81 0.03 0

14 44 30 <= Age < 45 68.622 Other Unknown 44500 34.791 No 378.88 0.15657 0

17 39 30 <= Age < 45 9 Tenant Employed 37500 38.779 Yes 664.51 0.25 1

20 52 45 <= Age < 60 51.442 Other Unknown 38500 12.297 Yes 1157.5 0.19273 0

21 37 30 <= Age < 45 10.343 Tenant Unknown 36500 23.314 No 732.28 0.065 1

22 51 45 <= Age < 60 12.087 Home Owner Employed 31500 27.971 Yes 437.95 0.01 0

24 43 30 <= Age < 45 40 Tenant Employed 33500 11.18 Yes 263.13 0.077267 0

⋮

[nf1, nxi1] = ksdensity(newTrainTbl.(predictor)(newTrainTbl.AgeGroup=='Age < 30')); [nf2, nxi2] = ksdensity(newTrainTbl.(predictor)(newTrainTbl.AgeGroup=='30 <= Age < 45')); [nf3, nxi3] = ksdensity(newTrainTbl.(predictor)(newTrainTbl.AgeGroup=='45 <= Age < 60')); [nf4, nxi4] = ksdensity(newTrainTbl.(predictor)(newTrainTbl.AgeGroup=='Age >= 60'));

Plot the original and the repaired distributions.

figure; tiledlayout(2,1) ax1 = nexttile; plot(xi1, f1, 'LineWidth', 1.5) hold on plot(xi2, f2, 'LineWidth', 1.5) plot(xi3, f3, 'LineWidth', 1.5) plot(xi4, f4, 'LineWidth', 1.5) legend(["Age < 30"; "30 <= Age < 45"; "45 <= Age < 60"; "Age >= 60"],'Location','northwest') ax1.Title.String = "Original Distribution of " + predictor; xlabel(predictor) ylabel('pdf') grid on ax2 = nexttile; plot(nxi1, nf1, 'LineWidth', 1.5) hold on plot(nxi2, nf2, 'LineWidth', 1.5) plot(nxi3, nf3, 'LineWidth', 1.5) plot(nxi4, nf4, 'LineWidth', 1.5) legend(["Age < 30"; "30 <= Age < 45"; "45 <= Age < 60"; "Age >= 60"],'Location','northwest') ax2.Title.String = "Repaired Distribution of " + predictor; xlabel(predictor) ylabel('pdf') grid on linkaxes([ax1, ax2], 'xy')

This plot demonstrates that the initial distributions of CustIncome of each group within the AgeGroup predictor are different. Younger people seem to have a lower income on average and more variation than older people. This difference introduces bias, which the fitted model then reflects. The disparateImpactRemover function modifies the data so that the distributions of all the subgroups are more similar. You see this distribution in the second subplot Repaired Distribution of CustIncome. Using this new data, you can fit a logistic regression model and then measure the model-level metrics and compare these with the model-level metrics from the original creditscorecard model (sc1).

New Credit Scoring Model

Use creditscorecard to create a creditscorecard object and use fitmodel to fit a credit scoring model with the new data (newTrainTbl). Then, you can compute model-level bias metrics using fairnessMetrics.

sc2 = creditscorecard(newTrainTbl,'IDVar','CustID', ... 'PredictorVars',PredictorVars,'ResponseVar','status'); sc2 = autobinning(sc2); sc2 = fitmodel(sc2,'VariableSelection','fullmodel');

Generalized linear regression model:

logit(status) ~ 1 + TmAtAddress + ResStatus + EmpStatus + CustIncome + TmWBank + OtherCC + AMBalance + UtilRate

Distribution = Binomial

Estimated Coefficients:

Estimate SE tStat pValue

_________ _______ _______ __________

(Intercept) 0.74041 0.07641 9.6899 3.327e-22

TmAtAddress 1.1658 0.87564 1.3313 0.18308

ResStatus 1.8719 1.2848 1.4569 0.14513

EmpStatus 0.88699 0.31991 2.7727 0.00556

CustIncome 0.98269 0.28725 3.421 0.00062396

TmWBank 1.1392 0.30677 3.7135 0.00020442

OtherCC 0.55005 2.0969 0.26231 0.79308

AMBalance 1.0478 0.3607 2.9049 0.0036734

UtilRate -0.071972 0.58704 -0.1226 0.90242

840 observations, 831 error degrees of freedom

Dispersion: 1

Chi^2-statistic vs. constant model: 50.4, p-value = 3.36e-08

Use displaypoints to compute the points per predictor per bin for the creditscorecard model (sc2).

pointsinfo2 = displaypoints(sc2)

pointsinfo2=35×3 table

Predictors Bin Points

_______________ _________________ _________

{'TmAtAddress'} {'[-Inf,9)' } -0.11003

{'TmAtAddress'} {'[9,15.1453)' } -0.091424

{'TmAtAddress'} {'[15.1453,Inf]'} 0.14546

{'TmAtAddress'} {'<missing>' } NaN

{'ResStatus' } {'Tenant' } -0.024878

{'ResStatus' } {'Home Owner' } 0.11858

{'ResStatus' } {'Other' } 0.30343

{'ResStatus' } {'<missing>' } NaN

{'EmpStatus' } {'Unknown' } -0.097539

{'EmpStatus' } {'Employed' } 0.3319

{'EmpStatus' } {'<missing>' } NaN

{'CustIncome' } {'[-Inf,31500)' } -0.30942

{'CustIncome' } {'[31500,38500)'} -0.09789

{'CustIncome' } {'[38500,45000)'} 0.21233

{'CustIncome' } {'[45000,Inf]' } 0.494

{'CustIncome' } {'<missing>' } NaN

⋮

Before computing probabilities of default with the test data, you need to transform the test data using the same transformation as for the training data. To make this transformation, use the transform method of the remover object and pass it in the data_Test data set. Then, use probdefault to compute the likelihood of default of the data_Test data set.

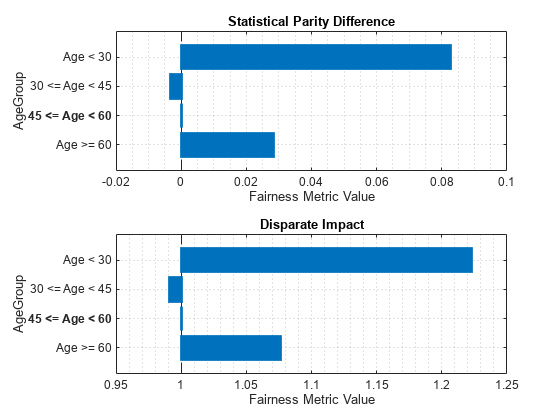

newTestTbl = transform(remover,data_Test); pd2 = probdefault(sc2,newTestTbl); predictions2 = double(pd2>threshold);

Use fairnessMetrics to compute fairness metrics at the model level and use report to generate a fairness metrics report.

modelMetrics2 = fairnessMetrics(newTestTbl,'status','Predictions',predictions2,'SensitiveAttributeNames','AgeGroup'); mmReport2 = report(modelMetrics2,'GroupMetrics','GroupCount')

mmReport2=4×8 table

ModelNames SensitiveAttributeNames Groups StatisticalParityDifference DisparateImpact EqualOpportunityDifference AverageAbsoluteOddsDifference GroupCount

__________ _______________________ ______________ ___________________________ _______________ __________________________ _____________________________ __________

Model1 AgeGroup Age < 30 0.082751 1.2226 0.18696 0.10408 22

Model1 AgeGroup 30 <= Age < 45 -0.0033738 0.99093 0.07902 0.076333 152

Model1 AgeGroup 45 <= Age < 60 0 1 0 0 156

Model1 AgeGroup Age >= 60 0.028205 1.0759 0.015528 0.026143 30

Use plot to visualize the statistical parity difference ('spd') and disparate impact ('di') bias metrics.

figure tiledlayout(2,1) nexttile plot(modelMetrics2,'spd') nexttile plot(modelMetrics2,'di')

Plot Disparate Impact and Accuracy for Different Repair Fraction Values

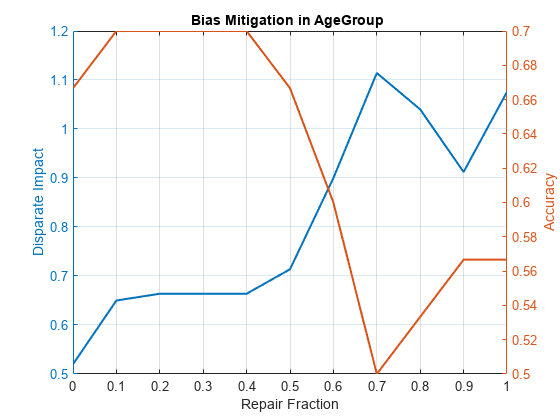

In this example, the bias mitigation process uses disparateImpactRemover to set RepairFraction = 1 in order to mitigate bias. However, it is useful to see how the disparate impact and accuracy varies with a change in the RepairFraction value. For example, use the AgeGroup predictor and plot the disparate impact and accuracy of the different subgroups for different values of RepairFraction.

subgroup =4; r = 0:0.1:1; Accuracy = zeros(11,1); di = zeros(11,1); for i = 0:1:10 [rmvr, trainTbl] = disparateImpactRemover(data_Train, 'AgeGroup' , ... 'PredictorNames', {'TmAtAddress','CustIncome','TmWBank','AMBalance','UtilRate'},'RepairFraction',i/10); testTbl = transform(rmvr, data_Test); sc = creditscorecard(trainTbl,'IDVar','CustID', ... 'PredictorVars',PredictorVars,'ResponseVar','status'); sc = autobinning(sc); sc = fitmodel(sc,'VariableSelection','fullmodel','Display','off'); pd = probdefault(sc,testTbl); predictions = double(pd>threshold); modelMetrics = fairnessMetrics(newTestTbl, 'status', 'Predictions', predictions, 'SensitiveAttributeNames','AgeGroup'); mmReport = report(modelMetrics,'BiasMetrics','di','GroupMetrics','accuracy'); di(i+1) = mmReport.DisparateImpact(subgroup); Accuracy(i+1) = mmReport.Accuracy(subgroup); end figure yyaxis left plot(r, di,'LineWidth', 1.5) title("Bias Mitigation in AgeGroup") xlabel("Repair Fraction") ylabel("Disparate Impact") yyaxis right plot(r, Accuracy,'LineWidth', 1.5) ylabel("Accuracy") grid on

If you select the subgroup 'Age < 30' from this plot, you can see that the accuracy increases as the RepairFraction value increases. Although this seems counterintuitive, looking further at the GroupCount of that age group in the mmReport2 table, this group has only 22 observations. This small number of observations explains the anomaly in this plot.

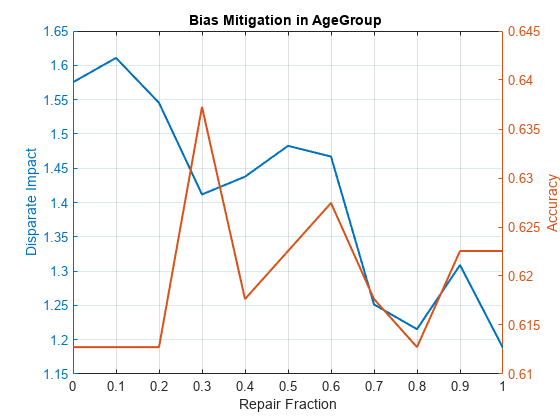

One way to mitigate this issue of not having enough data for a subgroup is to combine all unprivileged groups and compare them as one group against the privileged group. The following code shows you how by setting the majority group (45 <= Age < 60) as the privileged group and then by combining every other group into one and setting that group as the unprivileged group.

privilegedGroup = '45 <= Age < 60'; twoAgeGroups_TrainTbl = data_Train; twoAgeGroups_TrainTbl.AgeGroup = addcats(twoAgeGroups_TrainTbl.AgeGroup,'Other','After','Age >= 60'); twoAgeGroups_TrainTbl.AgeGroup(twoAgeGroups_TrainTbl.AgeGroup ~= privilegedGroup) = 'Other'; twoAgeGroups_TestTbl = data_Test; twoAgeGroups_TestTbl.AgeGroup = addcats(twoAgeGroups_TestTbl.AgeGroup,'Other','After','Age >= 60'); twoAgeGroups_TestTbl.AgeGroup(twoAgeGroups_TestTbl.AgeGroup ~= privilegedGroup) = 'Other'; r = 0:0.1:1; Accuracy = zeros(11,1); di = zeros(11,1); for i = 0:1:10 [rmvr, trainTbl] = disparateImpactRemover(twoAgeGroups_TrainTbl, 'AgeGroup' , ... 'PredictorNames', {'TmAtAddress','CustIncome','TmWBank','AMBalance','UtilRate'},'RepairFraction',i/10); testTbl = transform(rmvr, twoAgeGroups_TestTbl); sc = creditscorecard(trainTbl,'IDVar','CustID', ... 'PredictorVars',PredictorVars,'ResponseVar','status'); sc = autobinning(sc); sc = fitmodel(sc,'VariableSelection','fullmodel','Display','off'); pd = probdefault(sc,testTbl); predictions = double(pd>threshold); modelMetrics = fairnessMetrics(twoAgeGroups_TestTbl, 'status', 'Predictions', predictions, ... 'SensitiveAttributeNames','AgeGroup','ReferenceGroup','45 <= Age < 60'); mmReport = report(modelMetrics,'BiasMetrics','di','GroupMetrics','accuracy'); di(i+1) = mmReport.DisparateImpact(2); Accuracy(i+1) = mmReport.Accuracy(2); end figure yyaxis left plot(r, di,'LineWidth', 1.5) title('Bias Mitigation in AgeGroup ') xlabel('Repair Fraction') ylabel('Disparate Impact') yyaxis right plot(r, Accuracy,'LineWidth', 1.5) ylabel('Accuracy') grid on

You can use this privileged group and unprivileged group method if the goal is not to measure the bias of each individual group against the privileged group, but rather to measure the overall fairness of all customers who are not part of the privileged group.

References

[1] Nielsen, Aileen. "Chapter 4. Fairness PreProcessing." Practical Fairness. O'Reilly Media, Inc., Dec. 2020.

[2] Mehrabi, Ninareh, et al. “A Survey on Bias and Fairness in Machine Learning.” ArXiv:1908.09635 [Cs], Sept. 2019. arXiv.org, https://arxiv.org/abs/1908.09635.

[3] Wachter, Sandra, et al. Bias Preservation in Machine Learning: The Legality of Fairness Metrics Under EU Non-Discrimination Law. SSRN Scholarly Paper, ID 3792772, Social Science Research Network, 15 Jan. 2021. papers.ssrn.com, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3792772.

See Also

creditscorecard | autobinning | fitmodel | displaypoints | probdefault