predict

Compute conditional PD

Description

conditionalPD = predict(pdModel,data)

Examples

This example shows how to use fitLifetimePDModel to fit data with a Probit model and then predict the conditional probability of default (PD).

Load Data

Load the credit portfolio data.

load RetailCreditPanelData.mat

disp(head(data)) ID ScoreGroup YOB Default Year

__ __________ ___ _______ ____

1 Low Risk 1 0 1997

1 Low Risk 2 0 1998

1 Low Risk 3 0 1999

1 Low Risk 4 0 2000

1 Low Risk 5 0 2001

1 Low Risk 6 0 2002

1 Low Risk 7 0 2003

1 Low Risk 8 0 2004

disp(head(dataMacro))

Year GDP Market

____ _____ ______

1997 2.72 7.61

1998 3.57 26.24

1999 2.86 18.1

2000 2.43 3.19

2001 1.26 -10.51

2002 -0.59 -22.95

2003 0.63 2.78

2004 1.85 9.48

Join the two data components into a single data set.

data = join(data,dataMacro); disp(head(data))

ID ScoreGroup YOB Default Year GDP Market

__ __________ ___ _______ ____ _____ ______

1 Low Risk 1 0 1997 2.72 7.61

1 Low Risk 2 0 1998 3.57 26.24

1 Low Risk 3 0 1999 2.86 18.1

1 Low Risk 4 0 2000 2.43 3.19

1 Low Risk 5 0 2001 1.26 -10.51

1 Low Risk 6 0 2002 -0.59 -22.95

1 Low Risk 7 0 2003 0.63 2.78

1 Low Risk 8 0 2004 1.85 9.48

Partition Data

Separate the data into training and test partitions.

nIDs = max(data.ID); uniqueIDs = unique(data.ID); rng('default'); % for reproducibility c = cvpartition(nIDs,'HoldOut',0.4); TrainIDInd = training(c); TestIDInd = test(c); TrainDataInd = ismember(data.ID,uniqueIDs(TrainIDInd)); TestDataInd = ismember(data.ID,uniqueIDs(TestIDInd));

Create a Probit Lifetime PD Model

Use fitLifetimePDModel to create a Probit model.

pdModel = fitLifetimePDModel(data(TrainDataInd,:),"Probit",... 'AgeVar','YOB',... 'IDVar','ID',... 'LoanVars','ScoreGroup',... 'MacroVars',{'GDP','Market'},... 'ResponseVar','Default'); disp(pdModel)

Probit with properties:

ModelID: "Probit"

Description: ""

UnderlyingModel: [1×1 classreg.regr.CompactGeneralizedLinearModel]

IDVar: "ID"

AgeVar: "YOB"

LoanVars: "ScoreGroup"

MacroVars: ["GDP" "Market"]

ResponseVar: "Default"

WeightsVar: ""

TimeInterval: 1

Display the underlying model.

pdModel.UnderlyingModel

ans =

Compact generalized linear regression model:

probit(Default) ~ 1 + ScoreGroup + YOB + GDP + Market

Distribution = Binomial

Estimated Coefficients:

Estimate SE tStat pValue

__________ _________ _______ ___________

(Intercept) -1.6267 0.03811 -42.685 0

ScoreGroup_Medium Risk -0.26542 0.01419 -18.704 4.5503e-78

ScoreGroup_Low Risk -0.46794 0.016364 -28.595 7.775e-180

YOB -0.11421 0.0049724 -22.969 9.6208e-117

GDP -0.041537 0.014807 -2.8052 0.0050291

Market -0.0029609 0.0010618 -2.7885 0.0052954

388097 observations, 388091 error degrees of freedom

Dispersion: 1

Chi^2-statistic vs. constant model: 1.85e+03, p-value = 0

Predict on Training and Test Data

Predict the PD for training or test data sets.

DataSetChoice ="Training"; if DataSetChoice=="Training" Ind = TrainDataInd; else Ind = TestDataInd; end % Predict conditional PD PD = predict(pdModel,data(Ind,:)); head(data(Ind,:))

ID ScoreGroup YOB Default Year GDP Market

__ __________ ___ _______ ____ _____ ______

1 Low Risk 1 0 1997 2.72 7.61

1 Low Risk 2 0 1998 3.57 26.24

1 Low Risk 3 0 1999 2.86 18.1

1 Low Risk 4 0 2000 2.43 3.19

1 Low Risk 5 0 2001 1.26 -10.51

1 Low Risk 6 0 2002 -0.59 -22.95

1 Low Risk 7 0 2003 0.63 2.78

1 Low Risk 8 0 2004 1.85 9.48

disp(PD(1:8))

0.0095

0.0054

0.0045

0.0039

0.0036

0.0036

0.0017

0.0009

You can analyze and validate these predictions using modelDiscrimination and modelCalibration.

This example shows how to use fitLifetimePDModel to fit data with a Cox model and then predict the conditional probability of default (PD).

Load Data

Load the credit portfolio data.

load RetailCreditPanelData.mat

disp(head(data)) ID ScoreGroup YOB Default Year

__ __________ ___ _______ ____

1 Low Risk 1 0 1997

1 Low Risk 2 0 1998

1 Low Risk 3 0 1999

1 Low Risk 4 0 2000

1 Low Risk 5 0 2001

1 Low Risk 6 0 2002

1 Low Risk 7 0 2003

1 Low Risk 8 0 2004

disp(head(dataMacro))

Year GDP Market

____ _____ ______

1997 2.72 7.61

1998 3.57 26.24

1999 2.86 18.1

2000 2.43 3.19

2001 1.26 -10.51

2002 -0.59 -22.95

2003 0.63 2.78

2004 1.85 9.48

Join the two data components into a single data set.

data = join(data,dataMacro); disp(head(data))

ID ScoreGroup YOB Default Year GDP Market

__ __________ ___ _______ ____ _____ ______

1 Low Risk 1 0 1997 2.72 7.61

1 Low Risk 2 0 1998 3.57 26.24

1 Low Risk 3 0 1999 2.86 18.1

1 Low Risk 4 0 2000 2.43 3.19

1 Low Risk 5 0 2001 1.26 -10.51

1 Low Risk 6 0 2002 -0.59 -22.95

1 Low Risk 7 0 2003 0.63 2.78

1 Low Risk 8 0 2004 1.85 9.48

Partition Data

Separate the data into training and test partitions.

nIDs = max(data.ID); uniqueIDs = unique(data.ID); rng('default'); % for reproducibility c = cvpartition(nIDs,'HoldOut',0.4); TrainIDInd = training(c); TestIDInd = test(c); TrainDataInd = ismember(data.ID,uniqueIDs(TrainIDInd)); TestDataInd = ismember(data.ID,uniqueIDs(TestIDInd));

Create a Cox Lifetime PD Model

Use fitLifetimePDModel to create a Cox model.

ModelType ="cox"; pdModel = fitLifetimePDModel(data(TrainDataInd,:),ModelType,... 'IDVar','ID','AgeVar','YOB',... 'LoanVars','ScoreGroup','MacroVars',{'GDP' 'Market'},... 'ResponseVar','Default'); disp(pdModel)

Cox with properties:

ExtrapolationFactor: 1

ModelID: "Cox"

Description: ""

UnderlyingModel: [1×1 CoxModel]

IDVar: "ID"

AgeVar: "YOB"

LoanVars: "ScoreGroup"

MacroVars: ["GDP" "Market"]

ResponseVar: "Default"

WeightsVar: ""

TimeInterval: 1

Display the underlying model.

disp(pdModel.UnderlyingModel)

Cox Proportional Hazards regression model

Beta SE zStat pValue

__________ _________ _______ ___________

ScoreGroup_Medium Risk -0.6794 0.037029 -18.348 3.4442e-75

ScoreGroup_Low Risk -1.2442 0.045244 -27.501 1.7116e-166

GDP -0.084533 0.043687 -1.935 0.052995

Market -0.0084411 0.0032221 -2.6198 0.0087991

Log-likelihood: -41742.871

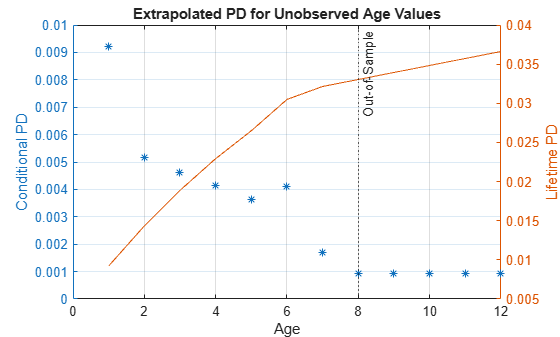

Predict on Age Values Not Observed in the Training Data

Cox models make predictions for the range of age values observed in the training data. To extrapolate for ages larger than the maximum age in the training data, an extrapolation rule is needed.

When using predict with a Cox model, you can set the ExtrapolationFactor property of the Cox model. By default, the ExtrapolationFactor is set to 1. For age values (AgeVar) greater than the maximum age observed in the training data, predict computes the conditional PD using the maximum age observed in the training data. In particular, the predicted PD value is constant if the predictor values do not change and only the age values change when the ExtrapolationFactor is 1.

To illustrate this, select the rows corresponding to a single ID and add new rows with new, incremental age values beyond the maximum observed age in the training data. The maximum age observed in the training data is 8; for illustration purposes, add rows with ages 9, 10, 11, and 12.

% Select rows corresponding to one ID % ID 1 goes from row 1 through 8 % Only the ID, Age (YOB) and predictor variables are needed dataNewAge = data(1:8,{'ID' 'YOB' 'ScoreGroup' 'GDP' 'Market'}); % Allocate more rows % This line copies the same predictor values going forward dataNewAge(9:12,:) = repmat(dataNewAge(8,:),4,1); % Reset age values to 9, 10, 11, 12 dataNewAge.YOB(9:12) = (9:12)'; % Show the new dataset disp(dataNewAge)

ID YOB ScoreGroup GDP Market

__ ___ __________ _____ ______

1 1 Low Risk 2.72 7.61

1 2 Low Risk 3.57 26.24

1 3 Low Risk 2.86 18.1

1 4 Low Risk 2.43 3.19

1 5 Low Risk 1.26 -10.51

1 6 Low Risk -0.59 -22.95

1 7 Low Risk 0.63 2.78

1 8 Low Risk 1.85 9.48

1 9 Low Risk 1.85 9.48

1 10 Low Risk 1.85 9.48

1 11 Low Risk 1.85 9.48

1 12 Low Risk 1.85 9.48

When the predictor values are constant in the rows with new age values and the extrapolation factor is 1, the predicted PD values are constant. If the extrapolation factor is set to a value smaller than 1, then the predicted PD values decrease more and more for larger age values and decrease towards zero exponentially.

% Extrapolation factor can be adjusted pdModel.ExtrapolationFactor =1; % Store predicted conditional PD in the same table dataNewAge.PD = predict(pdModel,dataNewAge); disp(dataNewAge)

ID YOB ScoreGroup GDP Market PD

__ ___ __________ _____ ______ __________

1 1 Low Risk 2.72 7.61 0.0092197

1 2 Low Risk 3.57 26.24 0.005158

1 3 Low Risk 2.86 18.1 0.0046079

1 4 Low Risk 2.43 3.19 0.0041351

1 5 Low Risk 1.26 -10.51 0.003645

1 6 Low Risk -0.59 -22.95 0.0041128

1 7 Low Risk 0.63 2.78 0.0017034

1 8 Low Risk 1.85 9.48 0.00092551

1 9 Low Risk 1.85 9.48 0.00092551

1 10 Low Risk 1.85 9.48 0.00092551

1 11 Low Risk 1.85 9.48 0.00092551

1 12 Low Risk 1.85 9.48 0.00092551

Also, it is useful to see the effect of the extrapolation factor on the lifetime prediction.

Plot the predicted conditional PD values and the lifetime PD values to see the effect of the extrapolation factor on both probabilities. The vertical dotted line separates the known age values (up to, and including, the age value 8), from the age values not observed in the training data (anything greater than 8). If the extrapolation factor is 1, the lifetime PD has a steady upward trend and the conditional PDs are constant. If the extrapolation factor is set to a smaller value like 0.5, the lifetime PD flattens quickly, as the conditional PD quickly drops towards zero.

dataNewAge.LifetimePD = predictLifetime(pdModel,dataNewAge); figure; yyaxis left plot(dataNewAge.YOB,dataNewAge.PD,'*') ylabel("Conditional PD") yyaxis right plot(dataNewAge.YOB,dataNewAge.LifetimePD) ylabel("Lifetime PD") title("Extrapolated PD for Unobserved Age Values") xlabel("Age") xline(8,':','Out-of-Sample') grid on

Input Arguments

Output Arguments

More About

References

[1] Baesens, Bart, Daniel Roesch, and Harald Scheule. Credit Risk Analytics: Measurement Techniques, Applications, and Examples in SAS. Wiley, 2016.

[2] Bellini, Tiziano. IFRS 9 and CECL Credit Risk Modelling and Validation: A Practical Guide with Examples Worked in R and SAS. San Diego, CA: Elsevier, 2019.

[3] Breeden, Joseph. Living with CECL: The Modeling Dictionary. Santa Fe, NM: Prescient Models LLC, 2018.

[4] Roesch, Daniel and Harald Scheule. Deep Credit Risk: Machine Learning with Python. Independently published, 2020.

Version History

Introduced in R2020bSee Also

modelDiscrimination | modelDiscriminationPlot | modelCalibration | modelCalibrationPlot | predictLifetime | fitLifetimePDModel | Logistic | Probit | Cox | customLifetimePDModel

Topics

- Basic Lifetime PD Model Validation

- Compare Logistic Model for Lifetime PD to Champion Model

- Compare Lifetime PD Models Using Cross-Validation

- Expected Credit Loss Computation

- Compare Model Discrimination and Model Calibration to Validate of Probability of Default

- Compare Probability of Default Using Through-the-Cycle and Point-in-Time Models

- Overview of Lifetime Probability of Default Models