customLifetimePDModel

Create customLifetimePDModel object for lifetime probability

of default

Since R2022b

Description

Create and analyze a customLifetimePDModel object to

calculate the lifetime probability of default (PD) using this workflow:

Fit a PD model that can predict PD for a loan or a portfolio of loans.

Define a function handle for a function that predicts the PD in your designated PD model.

Use

customLifetimePDModeland pass the specified function handle to create acustomLifetimePDModelobject. The designated model is now wrapped as a lifetime PD model.Use

predictto predict the conditional PD andpredictLifetimeto predict the lifetime PD.Use

modelDiscriminationto return AUROC and ROC data. You can plot the results usingmodelDiscriminationPlot.Use

modelCalibrationto return the RMSE of the observed and predicted PD data. You can plot the results usingmodelCalibrationPlot.

Creation

Syntax

Description

CustomLifetimePDModel = customLifetimePDModel(pdFcnHandle,IDVar=idvar_value,ResponseVar=responsevar_value)customLifetimePDModel object for a PD model

using required name-value arguments and sets model object properties.

CustomLifetimePDModel = customLifetimePDModel(___,Name=Value)CustomLifetimePDModel =

customLifetimePDModel(pdFcnHandle,IDVar="ID",AgeVar="YOB",Description="Scorecard

as lifetime PD

model",LoanVars="ScoreGroup",MacroVars={'GDP''Market'},ModelID="ScorecardLifetime",ResponseVar="Default",WeightsVar="Weights")

creates a CustomLifetimePDModel object.

Input Arguments

Name-Value Arguments

Properties

Object Functions

predict | Compute conditional PD |

predictLifetime | Compute cumulative lifetime PD, marginal PD, and survival probability |

modelDiscrimination | Compute AUROC and ROC data |

modelCalibration | Compute RMSE of predicted and observed PDs on grouped data |

modelDiscriminationPlot | Plot ROC curve |

modelCalibrationPlot | Plot observed default rates compared to predicted PDs on grouped data |

Examples

This example shows how to use the customLifetimePDModel object with a function handle to wrap a credit scorecard model as a customLifetimePDModel model.

Load Data

Load the credit portfolio data. The data set is in panel data format, with multiple rows per loan.

load RetailCreditPanelData.mat

disp(head(data)) ID ScoreGroup YOB Default Year

__ __________ ___ _______ ____

1 Low Risk 1 0 1997

1 Low Risk 2 0 1998

1 Low Risk 3 0 1999

1 Low Risk 4 0 2000

1 Low Risk 5 0 2001

1 Low Risk 6 0 2002

1 Low Risk 7 0 2003

1 Low Risk 8 0 2004

disp(head(dataMacro))

Year GDP Market

____ _____ ______

1997 2.72 7.61

1998 3.57 26.24

1999 2.86 18.1

2000 2.43 3.19

2001 1.26 -10.51

2002 -0.59 -22.95

2003 0.63 2.78

2004 1.85 9.48

Join the two data components into a single data set.

data = join(data,dataMacro); disp(head(data))

ID ScoreGroup YOB Default Year GDP Market

__ __________ ___ _______ ____ _____ ______

1 Low Risk 1 0 1997 2.72 7.61

1 Low Risk 2 0 1998 3.57 26.24

1 Low Risk 3 0 1999 2.86 18.1

1 Low Risk 4 0 2000 2.43 3.19

1 Low Risk 5 0 2001 1.26 -10.51

1 Low Risk 6 0 2002 -0.59 -22.95

1 Low Risk 7 0 2003 0.63 2.78

1 Low Risk 8 0 2004 1.85 9.48

Fit Credit Scorecard Model

Use creditscorecard to create a creditscorecard object, use autobinning to perform automatic binning of specified predictors, and then use fitmodel to fit a logistic regression model to weight of evidence (WOE) data. In this example, the entire data set is used to train the model.

sc = creditscorecard(data,'IDVar','ID','PredictorVars',{'ScoreGroup' 'YOB' 'GDP' 'Market'},'ResponseVar','Default'); sc = autobinning(sc); sc = autobinning(sc,'YOB','Algorithm','Split'); sc = fitmodel(sc,'Display','off'); displaypoints(sc)

ans=16×3 table

Predictors Bin Points

______________ _______________ _______

{'ScoreGroup'} {'High Risk' } 0.61102

{'ScoreGroup'} {'Medium Risk'} 1.3043

{'ScoreGroup'} {'Low Risk' } 1.9113

{'ScoreGroup'} {'<missing>' } NaN

{'YOB' } {'[-Inf,2)' } 0.56226

{'YOB' } {'[2,5)' } 1.0024

{'YOB' } {'[5,7)' } 1.4549

{'YOB' } {'[7,Inf]' } 2.509

{'YOB' } {'<missing>' } NaN

{'GDP' } {'[-Inf,0.63)'} 1.042

{'GDP' } {'[0.63,Inf]' } 1.1657

{'GDP' } {'<missing>' } NaN

{'Market' } {'[-Inf,2.78)'} 1.0731

{'Market' } {'[2.78,9.48)'} 1.1219

{'Market' } {'[9.48,Inf]' } 1.2294

{'Market' } {'<missing>' } NaN

Create customLifetimePDModel Object Using Function Handle

Use customLifetimePDModel with a function handle for the probdefault function.

pdFcnHandle = @(data) probdefault(sc,data); pdModel = customLifetimePDModel(pdFcnHandle,IDVar='ID',AgeVar='YOB', ... Description='Scorecard as lifetime PD model',LoanVars='ScoreGroup', ... MacroVars={'GDP' 'Market'},ModelID='ScorecardLifetime',ResponseVar='Default'); disp(pdModel)

CustomLifetimePD with properties:

ModelID: "ScorecardLifetime"

Description: "Scorecard as lifetime PD model"

UnderlyingModel: @(data)probdefault(sc,data)

IDVar: "ID"

AgeVar: "YOB"

LoanVars: "ScoreGroup"

MacroVars: ["GDP" "Market"]

ResponseVar: "Default"

WeightsVar: ""

TimeInterval: []

pdModel.UnderlyingModel

ans = function_handle with value:

@(data)probdefault(sc,data)

Predict Lifetime PD

Use the predictLifetime function to predict lifetime cumulative PD values for the first ID associated with the first eight rows of the data. The data input to predictLifetime must be in panel data form, with multiple rows per loan, and the function computes the cumulative probability of default for each period. For more information, see Time Interval and Data Input for Lifetime Prediction.

predictLifetime(pdModel,data(1:8,:))

ans = 8×1

0.0085

0.0134

0.0182

0.0236

0.0272

0.0312

0.0324

0.0335

Validate Model

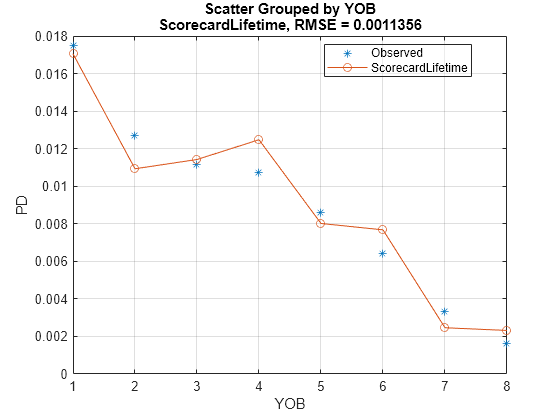

By wrapping the scorecard model as a lifetime PD model, all the validation functionality of the lifetime PD models is available. For example, use modelCalibrationPlot to visualize the observed default rates compared to the predicted probabilities of default.

modelCalibrationPlot(pdModel,data,'YOB')

References

[1] Baesens, Bart, Daniel Roesch, and Harald Scheule. Credit Risk Analytics: Measurement Techniques, Applications, and Examples in SAS. Wiley, 2016.

[2] Bellini, Tiziano. IFRS 9 and CECL Credit Risk Modelling and Validation: A Practical Guide with Examples Worked in R and SAS. San Diego, CA: Elsevier, 2019.

[3] Breeden, Joseph. Living with CECL: The Modeling Dictionary. Santa Fe, NM: Prescient Models LLC, 2018.

[4] Roesch, Daniel and Harald Scheule. Deep Credit Risk: Machine Learning with Python. Independently published, 2020.