mixsemiconjugateblm

Bayesian linear regression model with semiconjugate priors for stochastic search variable selection (SSVS)

Description

The Bayesian linear regression model object mixsemiconjugateblm

specifies the joint prior distribution of the regression coefficients and the disturbance

variance (β, σ2) for

implementing SSVS (see [1] and [2]) assuming β and

σ2 are dependent random

variables.

In general, when you create a Bayesian linear regression model object, it specifies the joint prior distribution and characteristics of the linear regression model only. That is, the model object is a template intended for further use. Specifically, to incorporate data into the model for posterior distribution analysis and feature selection, pass the model object and data to the appropriate object function.

Creation

Syntax

Description

PriorMdl = mixsemiconjugateblm(NumPredictors)PriorMdl) composed of

NumPredictors predictors and an intercept, and sets the

NumPredictors property. The joint prior distribution of

(β, σ2) is

appropriate for implementing SSVS for predictor selection [2]. PriorMdl

is a template that defines the prior distributions and the dimensionality of

β.

PriorMdl = mixsemiconjugateblm(NumPredictors,Name,Value)NumPredictors) using name-value pair arguments. Enclose each

property name in quotes. For example,

mixsemiconjugateblm(3,'Probability',abs(rand(4,1))) specifies

random prior regime probabilities for all four coefficients in the model.

Properties

Object Functions

estimate | Perform predictor variable selection for Bayesian linear regression models |

simulate | Simulate regression coefficients and disturbance variance of Bayesian linear regression model |

forecast | Forecast responses of Bayesian linear regression model |

plot | Visualize prior and posterior densities of Bayesian linear regression model parameters |

summarize | Distribution summary statistics of Bayesian linear regression model for predictor variable selection |

Examples

Consider the multiple linear regression model that predicts the US real gross national product (GNPR) using a linear combination of industrial production index (IPI), total employment (E), and real wages (WR).

For all , is a series of independent Gaussian disturbances with a mean of 0 and variance .

Assume these prior distributions for = 0,...,3:

, where and are independent, standard normal random variables. Therefore, the coefficients have a Gaussian mixture distribution. Assume all coefficients are conditionally independent, a priori.

. and are the shape and scale, respectively, of an inverse gamma distribution.

and it represents the random variable-inclusion regime variable with a discrete uniform distribution.

Create a prior model for SSVS. Specify the number of predictors p.

p = 3; PriorMdl = mixsemiconjugateblm(p);

PriorMdl is a mixsemiconjugateblm Bayesian linear regression model object representing the prior distribution of the regression coefficients and disturbance variance. mixsemiconjugateblm displays a summary of the prior distributions at the command line.

Alternatively, you can create a prior model for SSVS by passing the number of predictors to bayeslm and setting the ModelType name-value pair argument to 'mixsemiconjugate'.

MdlBayesLM = bayeslm(p,'ModelType','mixsemiconjugate')

MdlBayesLM =

mixsemiconjugateblm with properties:

NumPredictors: 3

Intercept: 1

VarNames: {4×1 cell}

Mu: [4×2 double]

V: [4×2 double]

Probability: [4×1 double]

Correlation: [4×4 double]

A: 3

B: 1

| Mean Std CI95 Positive Distribution

------------------------------------------------------------------------------

Intercept | 0 2.2472 [-5.201, 5.201] 0.500 Mixture distribution

Beta(1) | 0 2.2472 [-5.201, 5.201] 0.500 Mixture distribution

Beta(2) | 0 2.2472 [-5.201, 5.201] 0.500 Mixture distribution

Beta(3) | 0 2.2472 [-5.201, 5.201] 0.500 Mixture distribution

Sigma2 | 0.5000 0.5000 [ 0.138, 1.616] 1.000 IG(3.00, 1)

Mdl and MdlBayesLM are equivalent model objects.

You can set writable property values of created models using dot notation. Set the regression coefficient names to the corresponding variable names.

PriorMdl.VarNames = ["IPI" "E" "WR"]

PriorMdl =

mixsemiconjugateblm with properties:

NumPredictors: 3

Intercept: 1

VarNames: {4×1 cell}

Mu: [4×2 double]

V: [4×2 double]

Probability: [4×1 double]

Correlation: [4×4 double]

A: 3

B: 1

| Mean Std CI95 Positive Distribution

------------------------------------------------------------------------------

Intercept | 0 2.2472 [-5.201, 5.201] 0.500 Mixture distribution

IPI | 0 2.2472 [-5.201, 5.201] 0.500 Mixture distribution

E | 0 2.2472 [-5.201, 5.201] 0.500 Mixture distribution

WR | 0 2.2472 [-5.201, 5.201] 0.500 Mixture distribution

Sigma2 | 0.5000 0.5000 [ 0.138, 1.616] 1.000 IG(3.00, 1)

MATLAB® associates the variable names to the regression coefficients in displays.

Plot the prior distributions.

plot(PriorMdl);

The prior distribution of each coefficient is a mixture of two Gaussians: both components have a mean of zero, but component 1 has a large variance relative to component 2. Therefore, their distributions are centered at zero and have the spike-and-slab appearance.

Consider the linear regression model in Create Prior Model for SSVS.

Create a prior model for performing SSVS. Assume that and are independent (a semiconjugate mixture model). Specify the number of predictors p and the names of the regression coefficients.

p = 3; PriorMdl = mixsemiconjugateblm(p,'VarNames',["IPI" "E" "WR"]);

Display the prior regime probabilities and Gaussian mixture variance factors of the prior .

priorProbabilities = table(PriorMdl.Probability,'RowNames',PriorMdl.VarNames,... 'VariableNames',"Probability")

priorProbabilities=4×1 table

Probability

___________

Intercept 0.5

IPI 0.5

E 0.5

WR 0.5

priorV = array2table(PriorMdl.V,'RowNames',PriorMdl.VarNames,... 'VariableNames',["gammaIs1" "gammaIs0"])

priorV=4×2 table

gammaIs1 gammaIs0

________ ________

Intercept 10 0.1

IPI 10 0.1

E 10 0.1

WR 10 0.1

PriorMdl stores prior regime probabilities in the Probability property and the regime variance factors in the V property. The default prior probability of variable inclusion is 0.5. The default variance factors for each coefficient are 10 for the variable-inclusion regime and 0.01 for the variable-exclusion regime.

Load the Nelson-Plosser data set. Create variables for the response and predictor series.

load Data_NelsonPlosser X = DataTable{:,PriorMdl.VarNames(2:end)}; y = DataTable{:,'GNPR'};

Implement SSVS by estimating the marginal posterior distributions of and . Because SSVS uses Markov chain Monte Carlo (MCMC) for estimation, set a random number seed to reproduce the results.

rng(1); PosteriorMdl = estimate(PriorMdl,X,y);

Method: MCMC sampling with 10000 draws

Number of observations: 62

Number of predictors: 4

| Mean Std CI95 Positive Distribution Regime

-------------------------------------------------------------------------------

Intercept | -1.5629 2.6816 [-7.879, 2.703] 0.300 Empirical 0.5901

IPI | 4.6217 0.1222 [ 4.384, 4.865] 1.000 Empirical 1

E | 0.0004 0.0002 [ 0.000, 0.001] 0.976 Empirical 0.0918

WR | 2.6098 0.3691 [ 1.889, 3.347] 1.000 Empirical 1

Sigma2 | 50.9169 9.4955 [35.838, 72.707] 1.000 Empirical NaN

PosteriorMdl is an empiricalblm model object that stores draws from the posterior distributions of and given the data. estimate displays a summary of the marginal posterior distributions at the command line. Rows of the summary correspond to regression coefficients and the disturbance variance, and columns correspond to characteristics of the posterior distribution. The characteristics include:

CI95, which contains the 95% Bayesian equitailed credible intervals for the parameters. For example, the posterior probability that the regression coefficient ofEis in[0.000, 0.001]is 0.95.Regime, which contains the marginal posterior probability of variable inclusion ( for a variable). For example, the posterior probability thatEshould be included in the model is 0.0918.

Assuming that variables with Regime < 0.1 should be removed from the model, the results suggest that you can exclude the unemployment rate from the model.

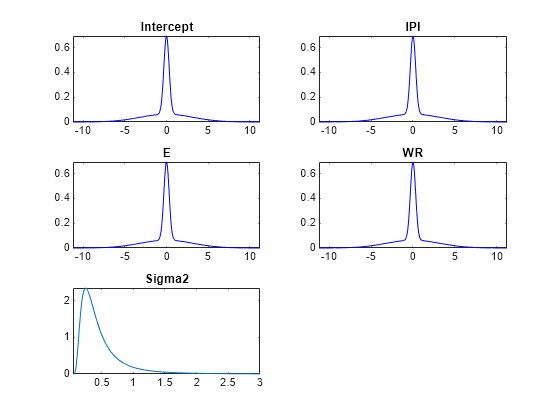

By default, estimate draws and discards a burn-in sample of size 5000. However, a good practice is to inspect a trace plot of the draws for adequate mixing and lack of transience. Plot a trace plot of the draws for each parameter. You can access the draws that compose the distribution (the properties BetaDraws and Sigma2Draws) using dot notation.

figure; for j = 1:(p + 1) subplot(2,2,j); plot(PosteriorMdl.BetaDraws(j,:)); title(sprintf('%s',PosteriorMdl.VarNames{j})); end

figure;

plot(PosteriorMdl.Sigma2Draws);

title('Sigma2');

The trace plots indicate that the draws seem to mix well. The plots show no detectable transience or serial correlation, and the draws do not jump between states.

Consider the linear regression model in Create Prior Model for SSVS.

Load the Nelson-Plosser data set. Create variables for the response and predictor series.

load Data_NelsonPlosser VarNames = ["IPI" "E" "WR"]; X = DataTable{:,VarNames}; y = DataTable{:,"GNPR"};

Assume the following:

The intercept is in the model with probability 0.9.

IPIandEare in the model with probability 0.75.If

Eis included in the model, then the probability thatWRis included in the model is 0.9.If

Eis excluded from the model, then the probability thatWRis included is 0.25.

Declare a function named priorssvsexample.m that:

Accepts a logical vector indicating whether the intercept and variables are in the model (

truefor model inclusion). Element 1 corresponds to the intercept, and the rest of the elements correspond to the variables in the data.Returns a numeric scalar representing the log of the described prior regime probability distribution.

function logprior = priorssvsexample(varinc) %PRIORSSVSEXAMPLE Log prior regime probability distribution for SSVS % PRIORSSVSEXAMPLE is an example of a custom log prior regime probability % distribution for SSVS with dependent random variables. varinc is % a 4-by-1 logical vector indicating whether 4 coefficients are in a model % and logPrior is a numeric scalar representing the log of the prior % distribution of the regime probabilities. % % Coefficients enter a model according to these rules: % * varinc(1) is included with probability 0.9. % * varinc(2) and varinc(3) are in the model with probability 0.75. % * If varinc(3) is included in the model, then the probability that % varinc(4) is included in the model is 0.9. % * If varinc(3) is excluded from the model, then the probability % that varinc(4) is included is 0.25. logprior = log(0.9) + 2*log(0.75) + log(varinc(3)*0.9 + (1-varinc(3))*0.25); end

Create a prior model for performing SSVS. Assume that  and

and  are independent (a semiconjugate mixture model). Specify the number of predictors

are independent (a semiconjugate mixture model). Specify the number of predictors p the names of the regression coefficients, and custom, prior probability distribution of the variable-inclusion regimes.

p = 3; PriorMdl = mixsemiconjugateblm(p,'VarNames',["IPI" "E" "WR"],... 'Probability',@priorssvsexample);

Implement SSVS by estimating the marginal posterior distributions of and . Because SSVS uses MCMC for estimation, set a random number seed to reproduce the results.

rng(1); PosteriorMdl = estimate(PriorMdl,X,y);

Method: MCMC sampling with 10000 draws

Number of observations: 62

Number of predictors: 4

| Mean Std CI95 Positive Distribution Regime

-------------------------------------------------------------------------------

Intercept | -1.4658 2.6046 [-7.781, 2.546] 0.308 Empirical 0.5516

IPI | 4.6227 0.1222 [ 4.385, 4.866] 1.000 Empirical 1

E | 0.0004 0.0002 [ 0.000, 0.001] 0.976 Empirical 0.2557

WR | 2.6105 0.3692 [ 1.886, 3.346] 1.000 Empirical 1

Sigma2 | 50.9621 9.4999 [35.860, 72.596] 1.000 Empirical NaN

Assuming, that variables with Regime < 0.1 should be removed from the model, the results suggest that you can include all variables in the model.

Consider the regression model in Create Prior Model for SSVS.

Perform SSVS:

Create a Bayesian regression model for SSVS with a semiconjugate prior for the data likelihood. Use the default settings.

Hold out the last 10 periods of data from estimation.

Estimate the marginal posterior distributions.

p = 3; PriorMdl = bayeslm(p,'ModelType','mixsemiconjugate','VarNames',["IPI" "E" "WR"]); load Data_NelsonPlosser fhs = 10; % Forecast horizon size X = DataTable{1:(end - fhs),PriorMdl.VarNames(2:end)}; y = DataTable{1:(end - fhs),'GNPR'}; XF = DataTable{(end - fhs + 1):end,PriorMdl.VarNames(2:end)}; % Future predictor data yFT = DataTable{(end - fhs + 1):end,'GNPR'}; % True future responses rng(1); % For reproducibility PosteriorMdl = estimate(PriorMdl,X,y,'Display',false);

Forecast responses using the posterior predictive distribution and the future predictor data XF. Plot the true values of the response and the forecasted values.

yF = forecast(PosteriorMdl,XF); figure; plot(dates,DataTable.GNPR); hold on plot(dates((end - fhs + 1):end),yF) h = gca; hp = patch([dates(end - fhs + 1) dates(end) dates(end) dates(end - fhs + 1)],... h.YLim([1,1,2,2]),[0.8 0.8 0.8]); uistack(hp,'bottom'); legend('Forecast Horizon','True GNPR','Forecasted GNPR','Location','NW') title('Real Gross National Product: 1909 - 1970'); ylabel('rGNP'); xlabel('Year'); hold off

yF is a 10-by-1 vector of future values of real GNP corresponding to the future predictor data.

Estimate the forecast root mean squared error (RMSE).

frmse = sqrt(mean((yF - yFT).^2))

frmse = 4.5935

The forecast RMSE is a relative measure of forecast accuracy. Specifically, you estimate several models using different assumptions. The model with the lowest forecast RMSE is the best-performing model of the ones being compared.

When you perform Bayesian regression with SSVS, a best practice is to tune the hyperparameters. One way to do so is to estimate the forecast RMSE over a grid of hyperparameter values, and choose the value that minimizes the forecast RMSE.

Copyright 2018 The MathWorks, Inc.

More About

Alternative Functionality

The bayeslm function can create any supported prior model object for Bayesian linear regression.

References

[1] George, E. I., and R. E. McCulloch. "Variable Selection Via Gibbs Sampling." Journal of the American Statistical Association. Vol. 88, No. 423, 1993, pp. 881–889.

[2] Koop, G., D. J. Poirier, and J. L. Tobias. Bayesian Econometric Methods. New York, NY: Cambridge University Press, 2007.

Version History

Introduced in R2018b