State-Space Models

A continuous state-space Markov process, or state-space model, allows for trajectories through a continuous state space. The underlying Markov process is typically unobserved. A supplemental observation equation describes the evolution of measurable characteristics of the system, dependent on the Markov process. State-space models specify the structure of unobserved dynamic processes, and the composition of the processes into observations. Econometrics Toolbox™ state-space functionality accommodates time-invariant or time-varying linear state-space models containing mean-zero Gaussian state disturbances and observation innovations. The initial state distributions can be stationary, constant, or diffuse. Functionalities enable you to alternatively take a Bayesian view of a standard state-space model. Bayesian models allow for richer representations, such as non-Gaussian state disturbances and observation innovations.

You can create a standard, diffuse, or Bayesian linear or nonlinear

state-space model using ssm, dssm, bssm, or bnlssm,

respectively.

For an overview of supported state-space model forms and to learn how to create a model in MATLAB®, see Create Continuous State-Space Models for Economic Data Analysis.

After creating a standard or diffuse model, you can, for example, estimate any unknown parameters using time series data, obtain filtered states, smooth states, generate forecasts, or characterize its dynamic behavior. To filter and smooth states, Econometrics Toolbox implements the standard or diffuse Kalman filter. For Bayesian models, you can draw samples from the posterior distribution using Markov chain Monte Carlo algorithms, such as the Metropolis-Hastings sampler.

Categories

- Standard State-Space Model

States with finite initial state variances

- Diffuse State-Space Model

States with infinite initial variances

- Bayesian State-Space Models

Posterior estimation, filtering, and simulation using custom prior models for standard and nonlinear state-space models

Featured Examples

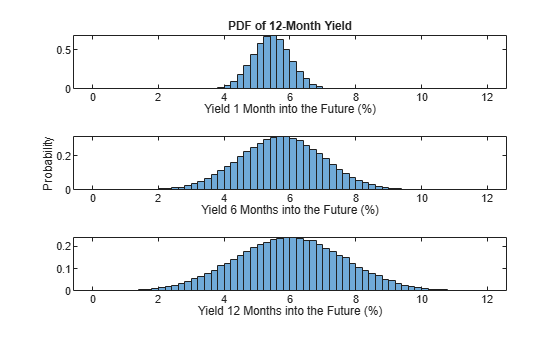

Apply State-Space Methodology to Analyze Diebold-Li Yield Curve Model

Use state-space models (SSM) and the Kalman filter to analyze the Diebold-Li yields-only and yields-macro models [2] of monthly yield-curve time series derived from U.S. Treasury bills and bonds. The analysis includes model estimation, simulation, smoothing, forecasting, and dynamic behavior characterization by applying Econometrics Toolbox™ SSM functionality. The example compares SSM estimation performance to the performance of more traditional econometric estimation techniques.

Analyze Linearized DSGE Models

Analyze a dynamic stochastic general equilibrium (DSGE) model using Bayesian state-space model tools.