Create Custom Lifetime PD Model for Credit Scorecard Model with Function Handle

This example shows how to use customLifetimePDModel to create a lifetime model for the probability of default. Using a retail credit data in panel format, you can create a credit scorecard model and then use a function handle with customLifetimePDModel to create a lifetime PD model.

Fit Credit Scorecard Model

Load the data set.

load RetailCreditPanelData.mat data = join(data,dataMacro); nIDs = max(data.ID); uniqueIDs = unique(data.ID); rng('default'); % for reproducibility c = cvpartition(nIDs,'HoldOut',0.4); TrainIDInd = training(c); TestIDInd = test(c); TrainDataInd = ismember(data.ID,uniqueIDs(TrainIDInd)); TestDataInd = ismember(data.ID,uniqueIDs(TestIDInd));

Use creditscorecard to create a creditscorecard object and then use autobinning to bin the data. Alternatively, you can bin the data using the Binning Explorer. You can fit the model using fitmodel.

sc = creditscorecard(data(TrainDataInd,:),'IDVar','ID','PredictorVars',{'ScoreGroup' 'YOB' 'GDP' 'Market'},'ResponseVar','Default')

sc =

creditscorecard with properties:

GoodLabel: 0

ResponseVar: 'Default'

WeightsVar: ''

VarNames: {'ID' 'ScoreGroup' 'YOB' 'Default' 'Year' 'GDP' 'Market'}

NumericPredictors: {'YOB' 'GDP' 'Market'}

CategoricalPredictors: {'ScoreGroup'}

BinMissingData: 0

IDVar: 'ID'

PredictorVars: {'ScoreGroup' 'YOB' 'GDP' 'Market'}

Data: [388097×7 table]

sc = autobinning(sc); sc = autobinning(sc,'YOB','Algorithm','Split'); sc = fitmodel(sc);

1. Adding ScoreGroup, Deviance = 42417.8562, Chi2Stat = 986.130141, PValue = 1.85820778e-216

2. Adding YOB, Deviance = 41644.7594, Chi2Stat = 773.096796, PValue = 3.81440566e-170

3. Adding Market, Deviance = 41616.8646, Chi2Stat = 27.8948108, PValue = 1.28092837e-07

4. Adding GDP, Deviance = 41612.2361, Chi2Stat = 4.62852205, PValue = 0.0314446396

Generalized linear regression model:

logit(Default) ~ 1 + ScoreGroup + YOB + GDP + Market

Distribution = Binomial

Estimated Coefficients:

Estimate SE tStat pValue

________ ________ ______ ___________

(Intercept) 4.6006 0.017273 266.35 0

ScoreGroup 0.98953 0.033117 29.88 3.5837e-196

YOB 1.0439 0.04216 24.76 2.4054e-135

GDP 4.5496 2.1012 2.1652 0.03037

Market 1.6892 0.44761 3.7738 0.00016076

388097 observations, 388092 error degrees of freedom

Dispersion: 1

Chi^2-statistic vs. constant model: 1.79e+03, p-value = 0

displaypoints(sc)

ans=16×3 table

Predictors Bin Points

______________ _______________ _______

{'ScoreGroup'} {'High Risk' } 0.61946

{'ScoreGroup'} {'Medium Risk'} 1.3073

{'ScoreGroup'} {'Low Risk' } 1.8816

{'ScoreGroup'} {'<missing>' } NaN

{'YOB' } {'[-Inf,2)' } 0.56097

{'YOB' } {'[2,5)' } 1.0021

{'YOB' } {'[5,7)' } 1.4673

{'YOB' } {'[7,Inf]' } 2.4996

{'YOB' } {'<missing>' } NaN

{'GDP' } {'[-Inf,0.63)'} 1.051

{'GDP' } {'[0.63,Inf]' } 1.1664

{'GDP' } {'<missing>' } NaN

{'Market' } {'[-Inf,2.78)'} 1.0661

{'Market' } {'[2.78,9.48)'} 1.1262

{'Market' } {'[9.48,Inf]' } 1.2358

{'Market' } {'<missing>' } NaN

Validate the creditscorecard model using validatemodel.

figure; s = validatemodel(sc,data(TestDataInd,:),'Plot','roc');

disp(s)

Measure Value

________________________ _______

{'Accuracy Ratio' } 0.39124

{'Area under ROC curve'} 0.69562

{'KS statistic' } 0.28409

{'KS score' } 4.6019

Wrap Credit Scorecard Model as Lifetime PD Model

Create a function handle for the probdefault function of the creditscorecard object. The only variable in the function handle (predictFcnHandle) is the data. The creditscorecard object (sc) is a fixed parameter of the probdefault function.

Use customLifetimePDModel to create an instance of a custom lifetime PD model using the function handle predictFcnHandle. Also, set up variable names for the model. The base class LifetimePDModel uses those variable names for different validations and computations.

predictFcnHandle = @(data)probdefault(sc,data); pdModel = customLifetimePDModel(predictFcnHandle,'ModelID','MyScorecardModel','IDVar','ID','AgeVar','YOB','LoanVars','ScoreGroup','MacroVars',{'GDP','Market'},'ResponseVar','Default')

pdModel =

CustomLifetimePD with properties:

ModelID: "MyScorecardModel"

Description: ""

UnderlyingModel: @(data)probdefault(sc,data)

IDVar: "ID"

AgeVar: "YOB"

LoanVars: "ScoreGroup"

MacroVars: ["GDP" "Market"]

ResponseVar: "Default"

WeightsVar: ""

TimeInterval: []

pdModel.UnderlyingModel

ans = function_handle with value:

@(data)probdefault(sc,data)

Predict and Validate Scores Using Custom Lifetime PD Model

You can use pdModel like any other lifetime PD model. The training and test data sets are in panel data format and can be passed to either predict or predictLifetime. The predict function returns the conditional PD, the same prediction as the probdefault function for the credit scorecard. The predictLifetime function returns the cumulative probability of default for each ID. Here, the first ID in the test data set spans the first eight rows. The conditional PD can go up or down, but the cumulative PD always increases from one period to the next.

CondPD = predict(pdModel,data(TestDataInd,:)); LifetimePD = predictLifetime(pdModel,data(TestDataInd,:)); disp([CondPD(1:8) LifetimePD(1:8)])

0.0154 0.0154

0.0089 0.0241

0.0089 0.0328

0.0099 0.0424

0.0066 0.0488

0.0075 0.0559

0.0022 0.0580

0.0020 0.0599

By wrapping the credit scorecard as a lifetime PD model object (pdModel), you can use all the validation capabilities of lifetime PD models are available. Use modelCalibrationPlot to plot observed default rates compared to the predicted PDs on grouped data.

figure;

modelCalibrationPlot(pdModel,data(TestDataInd,:),'YOB')

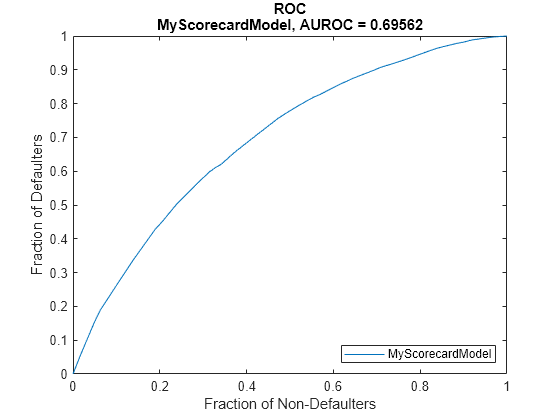

Use modelDiscriminationPlot to plot the ROC curve.

figure; modelDiscriminationPlot(pdModel,data(TestDataInd,:))

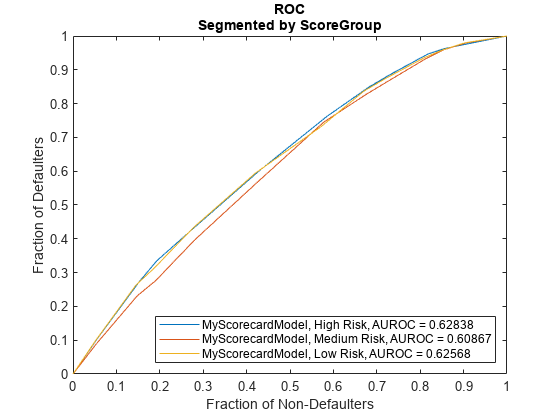

Use modelDiscriminationPlot to plot the ROC curve and segment the data by ScoreGroup.

figure; modelDiscriminationPlot(pdModel,data(TestDataInd,:),'SegmentBy','ScoreGroup')

See Also

customLifetimePDModel | fitLifetimePDModel | predict | predictLifetime | modelDiscrimination | modelDiscriminationPlot | modelCalibration | modelCalibrationPlot

Topics

- Create Custom Lifetime PD Model for Decision Tree Model with Function Handle

- Credit Scorecard Modeling with Missing Values

- Overview of Binning Explorer

- About Credit Scorecards

- Credit Scorecard Modeling Workflow