estimate

Estimate posterior distribution of Bayesian linear regression model parameters

Syntax

Description

PosteriorMdl = estimate(PriorMdl,X,y)PosteriorMdl that characterizes

the joint posterior distributions of the coefficients β and

the disturbance variance σ2.

PriorMdl specifies the joint prior distribution of the

parameters and the structure of the linear regression model.

X is the predictor data and y is the

response data. PriorMdl and PosteriorMdl

might not be the same object type.

To produce PosteriorMdl, the estimate

function updates the prior distribution with information about the parameters

that it obtains from the data.

NaNs in the data indicate missing values, which

estimate removes by using list-wise deletion.

PosteriorMdl = estimate(PriorMdl,X,y,Name,Value)

If you specify the Beta or Sigma2

name-value pair argument, then PosteriorMdl and

PriorMdl are equal.

[ uses any of the input argument combinations

in the previous syntaxes to return a table that contains the following for each

parameter: the posterior mean and standard deviation, 95% credible interval,

posterior probability that the parameter is greater than 0, and description of

the posterior distribution (if one exists). Also, the table contains the

posterior covariance matrix of β and

σ2. If you specify the

PosteriorMdl,Summary]

= estimate(___)Beta or Sigma2 name-value pair

argument, then estimate returns conditional posterior

estimates.

Examples

Consider a model that predicts the fuel economy (in MPG) of a car given its engine displacement and weight.

Load the carsmall data set.

load carsmall

x = [Displacement Weight];

y = MPG;Regress fuel economy onto engine displacement and weight, including an intercept to obtain ordinary least-squares (OLS) estimates.

Mdl = fitlm(x,y)

Mdl =

Linear regression model:

y ~ 1 + x1 + x2

Estimated Coefficients:

Estimate SE tStat pValue

__________ _________ _______ __________

(Intercept) 46.925 2.0858 22.497 6.0509e-39

x1 -0.014593 0.0082695 -1.7647 0.080968

x2 -0.0068422 0.0011337 -6.0353 3.3838e-08

Number of observations: 94, Error degrees of freedom: 91

Root Mean Squared Error: 4.09

R-squared: 0.747, Adjusted R-Squared: 0.741

F-statistic vs. constant model: 134, p-value = 7.22e-28

Mdl.MSE

ans = 16.7100

Create a default, diffuse prior distribution for one predictor.

p = 2; PriorMdl = bayeslm(p);

PriorMdl is a diffuseblm model object.

Use default options to estimate the posterior distribution.

PosteriorMdl = estimate(PriorMdl,x,y);

Method: Analytic posterior distributions

Number of observations: 94

Number of predictors: 3

| Mean Std CI95 Positive Distribution

--------------------------------------------------------------------------------

Intercept | 46.9247 2.1091 [42.782, 51.068] 1.000 t (46.92, 2.09^2, 91)

Beta(1) | -0.0146 0.0084 [-0.031, 0.002] 0.040 t (-0.01, 0.01^2, 91)

Beta(2) | -0.0068 0.0011 [-0.009, -0.005] 0.000 t (-0.01, 0.00^2, 91)

Sigma2 | 17.0855 2.5905 [12.748, 22.866] 1.000 IG(45.50, 0.0013)

PosteriorMdl is a conjugateblm model object.

The posterior means and the OLS coefficient estimates are almost identical. Also, the posterior standard deviations and OLS standard errors are almost identical. The posterior mean of Sigma2 is close to the OLS mean squared error (MSE).

Consider the multiple linear regression model that predicts the US real gross national product (GNPR) using a linear combination of total employment (E) and real wages (WR).

For all  ,

,  is a series of independent Gaussian disturbances with a mean of 0 and variance

is a series of independent Gaussian disturbances with a mean of 0 and variance  . Assume these prior distributions:

. Assume these prior distributions:

is a 3-D t distribution with 10 degrees of freedom for each component, correlation matrix

is a 3-D t distribution with 10 degrees of freedom for each component, correlation matrix C, locationct, and scalest. , with shape

, with shape  and scale

and scale  .

.

bayeslm treats these assumptions and the data likelihood as if the corresponding posterior is analytically intractable.

Declare a MATLAB® function that:

Accepts values of

and together in a column vector, and accepts values of the hyperparameters

and together in a column vector, and accepts values of the hyperparametersReturns the value of the joint prior distribution,

, given the values of and

, given the values of and

function logPDF = priorMVTIG(params,ct,st,dof,C,a,b) %priorMVTIG Log density of multivariate t times inverse gamma % priorMVTIG passes params(1:end-1) to the multivariate t density % function with dof degrees of freedom for each component and positive % definite correlation matrix C. priorMVTIG returns the log of the product of % the two evaluated densities. % % params: Parameter values at which the densities are evaluated, an % m-by-1 numeric vector. % % ct: Multivariate t distribution component centers, an (m-1)-by-1 % numeric vector. Elements correspond to the first m-1 elements % of params. % % st: Multivariate t distribution component scales, an (m-1)-by-1 % numeric (m-1)-by-1 numeric vector. Elements correspond to the % first m-1 elements of params. % % dof: Degrees of freedom for the multivariate t distribution, a % numeric scalar or (m-1)-by-1 numeric vector. priorMVTIG expands % scalars such that dof = dof*ones(m-1,1). Elements of dof % correspond to the elements of params(1:end-1). % % C: Correlation matrix for the multivariate t distribution, an % (m-1)-by-(m-1) symmetric, positive definite matrix. Rows and % columns correspond to the elements of params(1:end-1). % % a: Inverse gamma shape parameter, a positive numeric scalar. % % b: Inverse gamma scale parameter, a positive scalar. % beta = params(1:(end-1)); sigma2 = params(end); tVal = (beta - ct)./st; mvtDensity = mvtpdf(tVal,C,dof); igDensity = sigma2^(-a-1)*exp(-1/(sigma2*b))/(gamma(a)*b^a); logPDF = log(mvtDensity*igDensity); end

Create an anonymous function that operates like priorMVTIG, but accepts the parameter values only, and holds the hyperparameter values fixed at arbitrarily chosen values.

prednames = ["E" "WR"]; p = numel(prednames); numcoeff = p + 1; rng(1); % For reproducibility dof = 10; V = rand(numcoeff); Sigma = 0.5*(V + V') + numcoeff*eye(numcoeff); st = sqrt(diag(Sigma)); C = diag(1./st)*Sigma*diag(1./st); ct = rand(numcoeff,1); a = 10*rand; b = 10*rand; logPDF = @(params)priorMVTIG(params,ct,st,dof,C,a,b);

Create a custom joint prior model for the linear regression parameters. Specify the number of predictors p. Also, specify the function handle for priorMVTIG and the variable names.

PriorMdl = bayeslm(p,'ModelType','custom','LogPDF',logPDF,... 'VarNames',prednames);

PriorMdl is a customblm Bayesian linear regression model object representing the prior distribution of the regression coefficients and disturbance variance.

Load the Nelson-Plosser data set. Create variables for the response and predictor series.

load Data_NelsonPlosser X = DataTable{:,PriorMdl.VarNames(2:end)}; y = DataTable{:,"GNPR"};

Estimate the marginal posterior distributions of and using the Hamiltonian Monte Carlo (HMC) sampler. Specify drawing 10,000 samples and a burn-in period of 1000 draws.

PosteriorMdl = estimate(PriorMdl,X,y,'Sampler','hmc','NumDraws',1e4,... 'Burnin',1e3);

Method: MCMC sampling with 10000 draws

Number of observations: 62

Number of predictors: 3

| Mean Std CI95 Positive Distribution

------------------------------------------------------------------------------

Intercept | -3.6378 5.5852 [-15.849, 6.131] 0.254 Empirical

E | -0.0056 0.0006 [-0.007, -0.004] 0.000 Empirical

WR | 15.2496 0.7752 [13.716, 16.755] 1.000 Empirical

Sigma2 | 1285.6732 243.4374 [897.763, 1828.884] 1.000 Empirical

PosteriorMdl is an empiricalblm model object storing the draws from the posterior distributions.

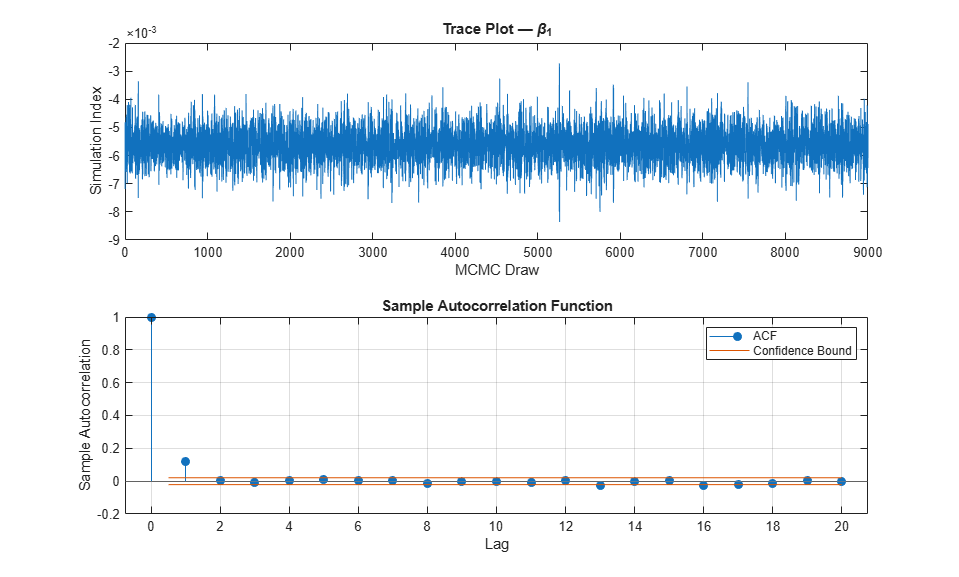

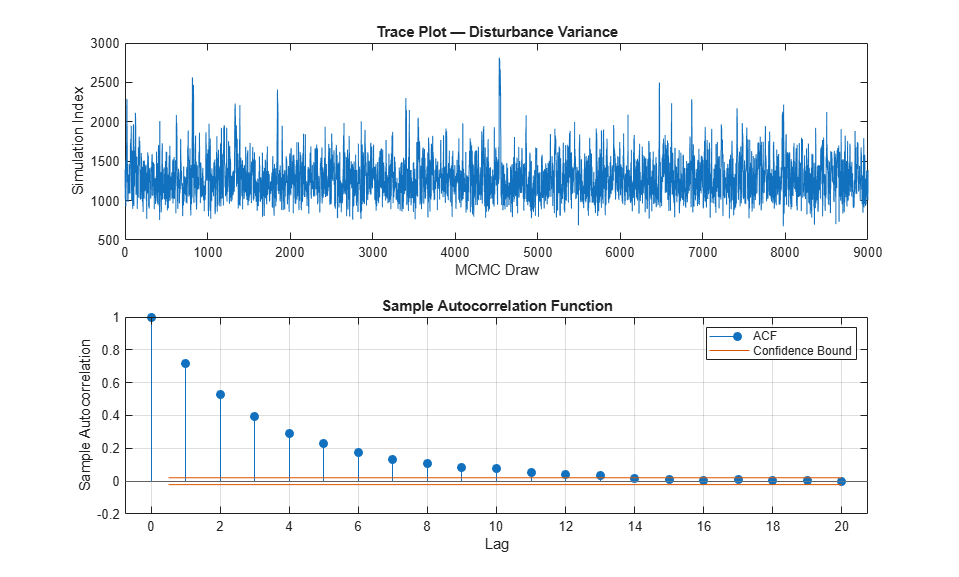

View a trace plot and an ACF plot of the draws from the posterior of  (for example) and the disturbance variance. Do not plot the burn-in period.

(for example) and the disturbance variance. Do not plot the burn-in period.

figure; subplot(2,1,1) plot(PosteriorMdl.BetaDraws(2,1001:end)); title(['Trace Plot ' char(8212) ' \beta_1']); xlabel('MCMC Draw') ylabel('Simulation Index') subplot(2,1,2) autocorr(PosteriorMdl.BetaDraws(2,1001:end)) figure; subplot(2,1,1) plot(PosteriorMdl.Sigma2Draws(1001:end)); title(['Trace Plot ' char(8212) ' Disturbance Variance']); xlabel('MCMC Draw') ylabel('Simulation Index') subplot(2,1,2) autocorr(PosteriorMdl.Sigma2Draws(1001:end))

The MCMC sample of the disturbance variance appears to mix well.

Consider the regression model in Estimate Posterior Using Hamiltonian Monte Carlo Sampler. This example uses the same data and context, but assumes a diffuse prior model instead.

Create a diffuse prior model for the linear regression parameters. Specify the number of predictors p and the names of the regression coefficients.

p = 3; PriorMdl = bayeslm(p,'ModelType','diffuse','VarNames',["IPI" "E" "WR"])

PriorMdl =

diffuseblm with properties:

NumPredictors: 3

Intercept: 1

VarNames: {4×1 cell}

| Mean Std CI95 Positive Distribution

-----------------------------------------------------------------------------

Intercept | 0 Inf [ NaN, NaN] 0.500 Proportional to one

IPI | 0 Inf [ NaN, NaN] 0.500 Proportional to one

E | 0 Inf [ NaN, NaN] 0.500 Proportional to one

WR | 0 Inf [ NaN, NaN] 0.500 Proportional to one

Sigma2 | Inf Inf [ NaN, NaN] 1.000 Proportional to 1/Sigma2

PriorMdl is a diffuseblm model object.

Load the Nelson-Plosser data set. Create variables for the response and predictor series.

load Data_NelsonPlosser X = DataTable{:,PriorMdl.VarNames(2:end)}; y = DataTable{:,'GNPR'};

Estimate the conditional posterior distribution of given the data and that , and return the estimation summary table to access the estimates.

[Mdl,SummaryBeta] = estimate(PriorMdl,X,y,'Sigma2',2);Method: Analytic posterior distributions

Conditional variable: Sigma2 fixed at 2

Number of observations: 62

Number of predictors: 4

| Mean Std CI95 Positive Distribution

--------------------------------------------------------------------------------

Intercept | -24.2536 1.8696 [-27.918, -20.589] 0.000 N (-24.25, 1.87^2)

IPI | 4.3913 0.0301 [ 4.332, 4.450] 1.000 N (4.39, 0.03^2)

E | 0.0011 0.0001 [ 0.001, 0.001] 1.000 N (0.00, 0.00^2)

WR | 2.4682 0.0743 [ 2.323, 2.614] 1.000 N (2.47, 0.07^2)

Sigma2 | 2 0 [ 2.000, 2.000] 1.000 Fixed value

estimate displays a summary of the conditional posterior distribution of . Because is fixed at 2 during estimation, inferences on it are trivial.

Extract the mean vector and covariance matrix of the conditional posterior of from the estimation summary table.

condPostMeanBeta = SummaryBeta.Mean(1:(end - 1))

condPostMeanBeta = 4×1

-24.2536

4.3913

0.0011

2.4682

CondPostCovBeta = SummaryBeta.Covariances(1:(end - 1),1:(end - 1))

CondPostCovBeta = 4×4

3.4956 0.0350 -0.0001 0.0241

0.0350 0.0009 -0.0000 -0.0013

-0.0001 -0.0000 0.0000 -0.0000

0.0241 -0.0013 -0.0000 0.0055

Display Mdl.

Mdl

Mdl =

diffuseblm with properties:

NumPredictors: 3

Intercept: 1

VarNames: {4×1 cell}

| Mean Std CI95 Positive Distribution

-----------------------------------------------------------------------------

Intercept | 0 Inf [ NaN, NaN] 0.500 Proportional to one

IPI | 0 Inf [ NaN, NaN] 0.500 Proportional to one

E | 0 Inf [ NaN, NaN] 0.500 Proportional to one

WR | 0 Inf [ NaN, NaN] 0.500 Proportional to one

Sigma2 | Inf Inf [ NaN, NaN] 1.000 Proportional to 1/Sigma2

Because estimate computes the conditional posterior distribution, it returns the original prior model, not the posterior, in the first position of the output argument list.

Estimate the conditional posterior distributions of given that is condPostMeanBeta.

[~,SummarySigma2] = estimate(PriorMdl,X,y,'Beta',condPostMeanBeta);Method: Analytic posterior distributions

Conditional variable: Beta fixed at -24.2536 4.3913 0.00112035 2.46823

Number of observations: 62

Number of predictors: 4

| Mean Std CI95 Positive Distribution

--------------------------------------------------------------------------------

Intercept | -24.2536 0 [-24.254, -24.254] 0.000 Fixed value

IPI | 4.3913 0 [ 4.391, 4.391] 1.000 Fixed value

E | 0.0011 0 [ 0.001, 0.001] 1.000 Fixed value

WR | 2.4682 0 [ 2.468, 2.468] 1.000 Fixed value

Sigma2 | 48.5138 9.0088 [33.984, 69.098] 1.000 IG(31.00, 0.00069)

estimate displays a summary of the conditional posterior distribution of . Because is fixed to condPostMeanBeta during estimation, inferences on it are trivial.

Extract the mean and variance of the conditional posterior of from the estimation summary table.

condPostMeanSigma2 = SummarySigma2.Mean(end)

condPostMeanSigma2 = 48.5138

CondPostVarSigma2 = SummarySigma2.Covariances(end,end)

CondPostVarSigma2 = 81.1581

Consider the regression model in Estimate Posterior Using Hamiltonian Monte Carlo Sampler. This example uses the same data and context, but assumes a semiconjugate prior model instead.

Create a semiconjugate prior model for the linear regression parameters. Specify the number of predictors p and the names of the regression coefficients.

p = 3; PriorMdl = bayeslm(p,'ModelType','semiconjugate',... 'VarNames',["IPI" "E" "WR"]);

PriorMdl is a semiconjugateblm model object.

Load the Nelson-Plosser data set. Create variables for the response and predictor series.

load Data_NelsonPlosser X = DataTable{:,PriorMdl.VarNames(2:end)}; y = DataTable{:,'GNPR'};

Estimate the marginal posterior distributions of and .

rng(1); % For reproducibility

[PosteriorMdl,Summary] = estimate(PriorMdl,X,y);Method: Gibbs sampling with 10000 draws

Number of observations: 62

Number of predictors: 4

| Mean Std CI95 Positive Distribution

-------------------------------------------------------------------------

Intercept | -23.9922 9.0520 [-41.734, -6.198] 0.005 Empirical

IPI | 4.3929 0.1458 [ 4.101, 4.678] 1.000 Empirical

E | 0.0011 0.0003 [ 0.000, 0.002] 0.999 Empirical

WR | 2.4711 0.3576 [ 1.762, 3.178] 1.000 Empirical

Sigma2 | 46.7474 8.4550 [33.099, 66.126] 1.000 Empirical

PosteriorMdl is an empiricalblm model object because marginal posterior distributions of semiconjugate models are analytically intractable, so estimate must implement a Gibbs sampler. Summary is a table containing the estimates and inferences that estimate displays at the command line.

Display the summary table.

Summary

Summary=5×6 table

Mean Std CI95 Positive Distribution Covariances

_________ __________ ________________________ ________ _____________ ______________________________________________________________________

Intercept -23.992 9.052 -41.734 -6.1976 0.0053 {'Empirical'} 81.938 0.81622 -0.0025308 0.58928 0

IPI 4.3929 0.14578 4.1011 4.6782 1 {'Empirical'} 0.81622 0.021252 -7.1663e-06 -0.030939 0

E 0.0011124 0.00033976 0.00045128 0.0017883 0.9989 {'Empirical'} -0.0025308 -7.1663e-06 1.1544e-07 -8.4598e-05 0

WR 2.4711 0.3576 1.7622 3.1781 1 {'Empirical'} 0.58928 -0.030939 -8.4598e-05 0.12788 0

Sigma2 46.747 8.455 33.099 66.126 1 {'Empirical'} 0 0 0 0 71.487

Access the 95% equitailed credible interval of the regression coefficient of IPI.

Summary.CI95(2,:)

ans = 1×2

4.1011 4.6782

Input Arguments

Name-Value Arguments

Output Arguments

Limitations

If PriorMdl is an empiricalblm model object. You cannot specify Beta or

Sigma2. You cannot estimate conditional posterior distributions

by using an empirical prior distribution.

More About

Tips

Monte Carlo simulation is subject to variation. If

estimateuses Monte Carlo simulation, then estimates and inferences might vary when you callestimatemultiple times under seemingly equivalent conditions. To reproduce estimation results, set a random number seed by usingrngbefore callingestimate.If

estimateissues an error while estimating the posterior distribution using a custom prior model, then try adjusting initial parameter values by usingBetaStartorSigma2Start, or try adjusting the declared log prior function, and then reconstructing the model. The error might indicate that the log of the prior distribution is–Infat the specified initial values.

Algorithms

Whenever the prior distribution (

PriorMdl) and the data likelihood yield an analytically tractable posterior distribution,estimateevaluates the closed-form solutions to Bayes estimators. Otherwise,estimateresorts to Monte Carlo simulation to estimate parameters and draw inferences. For more details, see Posterior Estimation and Inference.This figure illustrates how

estimatereduces the Monte Carlo sample using the values ofNumDraws,Thin, andBurnIn. Rectangles represent successive draws from the distribution.estimateremoves the white rectangles from the Monte Carlo sample. The remainingNumDrawsblack rectangles compose the Monte Carlo sample.